pacman::p_load(tidyverse, tsibble, feasts, fable, seasonal)19 Visualising, Analysing and Forecasting Time-series Data: tidyverts methods

19.1 Learning Outcome

tidyverts is a family of R packages specially designed for visualising, analysing and forecasting time-series data conforming to tidyverse framework. It is the work of Dr. Rob Hyndman, professor of statistics at Monash University, and his team. The family of R packages are intended to be the next-generation replacement for the very popular forecast package, and is currently under active development.

The main reference for tidyverts is the textbook Forecasting: Principles and Practice, 3rd Edition, by Hyndman and Athanasopoulos. It’s highly recommended to read that in conjunction with working through the notebooks here.

By the end of this session, you will be able to:

- import and wrangling time-series data by using appropriate tidyverse methods,

- visualise and analyse time-series data,

- calibrate time-series forecasting models by using exponential smoothing and ARIMA techniques, and

- compare and evaluate the performance of forecasting models.

19.2 Getting Started

For the purpose of this hands-on exercise, the following R packages will be used.

- lubridate provides a collection to functions to parse and wrangle time and date data.

- tsibble, feasts, fable and fable.prophet are belong to tidyverts, a family of tidy tools for time series data handling, analysis and forecasting.

- tsibble provides a data infrastructure for tidy temporal data with wrangling tools. Adapting the tidy data principles, tsibble is a data- and model-oriented object.

- feasts provides a collection of tools for the analysis of time series data. The package name is an acronym comprising of its key features: Feature Extraction And Statistics for Time Series.

19.2.1 Importing the data

First, read_csv() of readr package is used to import visitor_arrivals_by_air.csv file into R environment. The imported file is saved an tibble object called ts_data.

ts_data <- read_csv(

"data/visitor_arrivals_by_air.csv")In the code chunk below, dmy() of lubridate package is used to convert data type of Month-Year field from Character to Date.

ts_data$`Month-Year` <- dmy(

ts_data$`Month-Year`)19.2.2 Conventional base ts object versus tibble object

tibble object

ts_data# A tibble: 144 × 34

`Month-Year` `Republic of South Africa` Canada USA Bangladesh Brunei China

<date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 2008-01-01 3680 6972 31155 6786 3729 79599

2 2008-02-01 1662 6056 27738 6314 3070 82074

3 2008-03-01 3394 6220 31349 7502 4805 72546

4 2008-04-01 3337 4764 26376 7333 3096 76112

5 2008-05-01 2089 4460 26788 7988 3586 64808

6 2008-06-01 2515 3888 29725 8301 5284 55238

7 2008-07-01 2919 5313 33183 9004 4070 80747

8 2008-08-01 2471 4519 27427 7913 4183 66625

9 2008-09-01 2492 3421 21588 7549 3160 52649

10 2008-10-01 3023 4756 25112 7527 2983 54423

# ℹ 134 more rows

# ℹ 27 more variables: `Hong Kong SAR (China)` <dbl>, India <dbl>,

# Indonesia <dbl>, Japan <dbl>, `South Korea` <dbl>, Kuwait <dbl>,

# Malaysia <dbl>, Myanmar <dbl>, Pakistan <dbl>, Philippines <dbl>,

# `Saudi Arabia` <dbl>, `Sri Lanka` <dbl>, Taiwan <dbl>, Thailand <dbl>,

# `United Arab Emirates` <dbl>, Vietnam <dbl>, `Belgium & Luxembourg` <dbl>,

# Finland <dbl>, France <dbl>, Germany <dbl>, Italy <dbl>, …19.2.3 Conventional base ts object versus tibble object

ts object

ts_data_ts <- ts(ts_data)

head(ts_data_ts) Month-Year Republic of South Africa Canada USA Bangladesh Brunei China

[1,] 13879 3680 6972 31155 6786 3729 79599

[2,] 13910 1662 6056 27738 6314 3070 82074

[3,] 13939 3394 6220 31349 7502 4805 72546

[4,] 13970 3337 4764 26376 7333 3096 76112

[5,] 14000 2089 4460 26788 7988 3586 64808

[6,] 14031 2515 3888 29725 8301 5284 55238

Hong Kong SAR (China) India Indonesia Japan South Korea Kuwait Malaysia

[1,] 17103 41639 62683 37673 27937 284 31352

[2,] 21089 37170 47834 35297 22633 241 35030

[3,] 23230 44815 64688 42575 22876 206 37629

[4,] 17688 49527 58074 26839 20634 193 37521

[5,] 19340 67754 57089 30814 22785 140 38044

[6,] 19152 57380 70118 31001 22575 354 40419

Myanmar Pakistan Philippines Saudi Arabia Sri Lanka Taiwan Thailand

[1,] 5269 1395 18622 406 5289 13757 18370

[2,] 4643 1027 21609 591 4767 13921 16400

[3,] 6218 1635 28464 626 4988 11181 23387

[4,] 7324 1232 30131 644 7639 11665 24469

[5,] 5395 1306 30193 470 5125 11436 21935

[6,] 5542 1996 25800 772 4791 10689 19900

United Arab Emirates Vietnam Belgium & Luxembourg Finland France Germany

[1,] 2652 10315 1341 1179 6918 11982

[2,] 2230 13415 1449 1207 7876 13256

[3,] 3353 14320 1674 1071 8066 15185

[4,] 3245 15413 1426 768 8312 11604

[5,] 2856 14424 1243 690 7066 9853

[6,] 4292 21368 1255 624 5926 9347

Italy Netherlands Spain Switzerland United Kingdom Australia New Zealand

[1,] 2953 4938 1668 4450 41934 71260 7806

[2,] 2704 4885 1568 4381 44029 45595 4729

[3,] 2822 5015 2254 5015 49489 53191 6106

[4,] 3018 4902 1503 5434 35771 56514 7560

[5,] 2165 4397 1365 4427 24464 57808 9090

[6,] 2022 4166 1446 3359 22473 63350 968119.2.4 Converting tibble object to tsibble object

Built on top of the tibble, a tsibble (or tbl_ts) is a data- and model-oriented object. Compared to the conventional time series objects in R, for example ts, zoo, and xts, the tsibble preserves time indices as the essential data column and makes heterogeneous data structures possible. Beyond the tibble-like representation, key comprised of single or multiple variables is introduced to uniquely identify observational units over time (index).

The code chunk below converting ts_data from tibble object into tsibble object by using as_tsibble() of tsibble R package.

ts_tsibble <- ts_data %>%

mutate(Month = yearmonth(`Month-Year`)) %>%

as_tsibble(index = `Month`)What can we learn from the code chunk above? + mutate() of dplyr package is used to derive a new field by transforming the data values in Month-Year field into month-year format. The transformation is performed by using yearmonth() of tsibble package. + as_tsibble() is used to convert the tibble data frame into tsibble data frame.

19.2.5 tsibble object

ts_tsibble# A tsibble: 144 x 35 [1M]

`Month-Year` `Republic of South Africa` Canada USA Bangladesh Brunei China

<date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 2008-01-01 3680 6972 31155 6786 3729 79599

2 2008-02-01 1662 6056 27738 6314 3070 82074

3 2008-03-01 3394 6220 31349 7502 4805 72546

4 2008-04-01 3337 4764 26376 7333 3096 76112

5 2008-05-01 2089 4460 26788 7988 3586 64808

6 2008-06-01 2515 3888 29725 8301 5284 55238

7 2008-07-01 2919 5313 33183 9004 4070 80747

8 2008-08-01 2471 4519 27427 7913 4183 66625

9 2008-09-01 2492 3421 21588 7549 3160 52649

10 2008-10-01 3023 4756 25112 7527 2983 54423

# ℹ 134 more rows

# ℹ 28 more variables: `Hong Kong SAR (China)` <dbl>, India <dbl>,

# Indonesia <dbl>, Japan <dbl>, `South Korea` <dbl>, Kuwait <dbl>,

# Malaysia <dbl>, Myanmar <dbl>, Pakistan <dbl>, Philippines <dbl>,

# `Saudi Arabia` <dbl>, `Sri Lanka` <dbl>, Taiwan <dbl>, Thailand <dbl>,

# `United Arab Emirates` <dbl>, Vietnam <dbl>, `Belgium & Luxembourg` <dbl>,

# Finland <dbl>, France <dbl>, Germany <dbl>, Italy <dbl>, …19.3 Visualising Time-series Data

In order to visualise the time-series data effectively, we need to organise the data frame from wide to long format by using pivot_longer() of tidyr package as shown below.

ts_longer <- ts_data %>%

pivot_longer(cols = c(2:34),

names_to = "Country",

values_to = "Arrivals")19.3.1 Visualising single time-series: ggplot2 methods

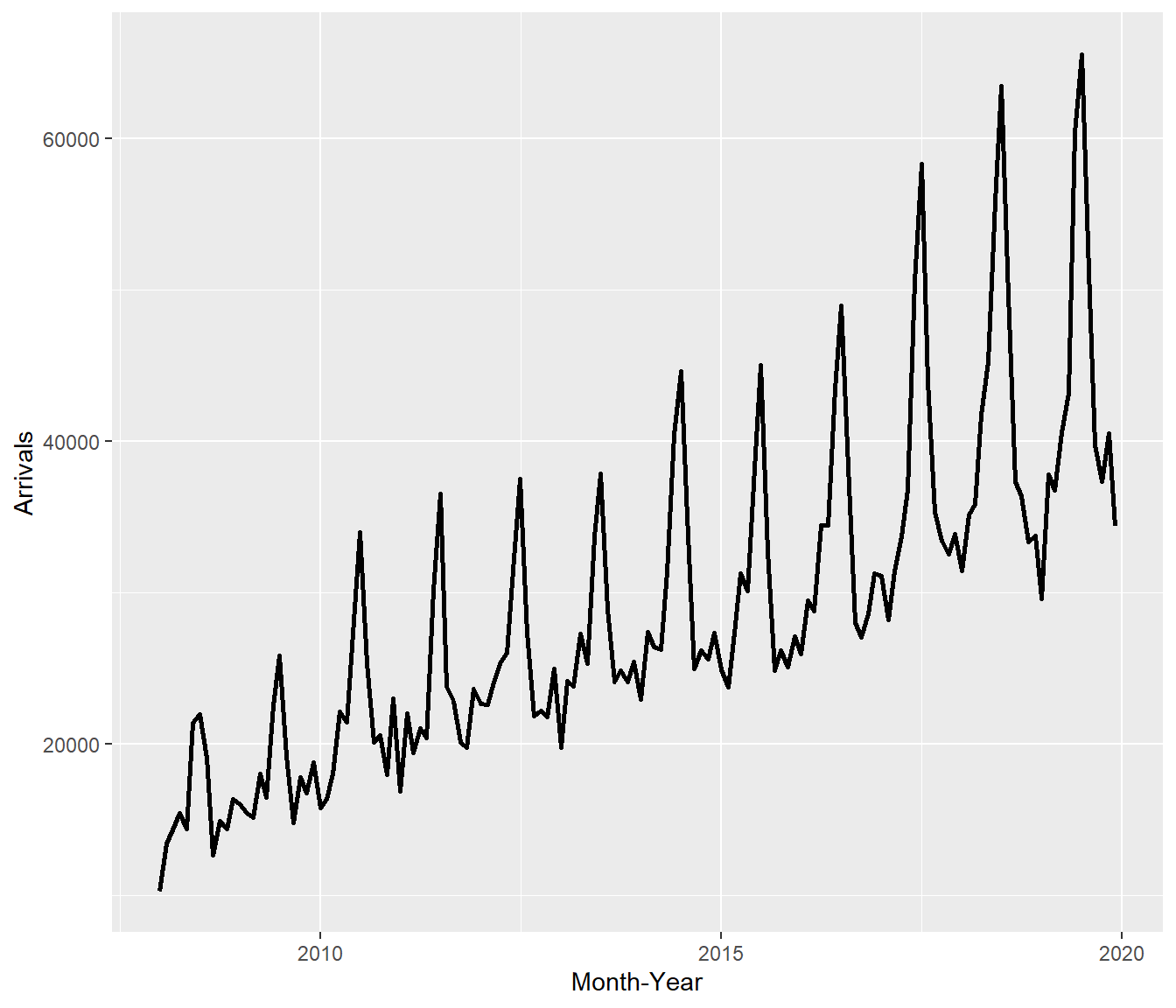

ts_longer %>%

filter(Country == "Vietnam") %>%

ggplot(aes(x = `Month-Year`,

y = Arrivals))+

geom_line(size = 0.5)What can we learn from the code chunk above?

filter()of dplyr package is used to select records belong to Vietnam.geom_line()of ggplot2 package is used to plot the time-series line graph. ]

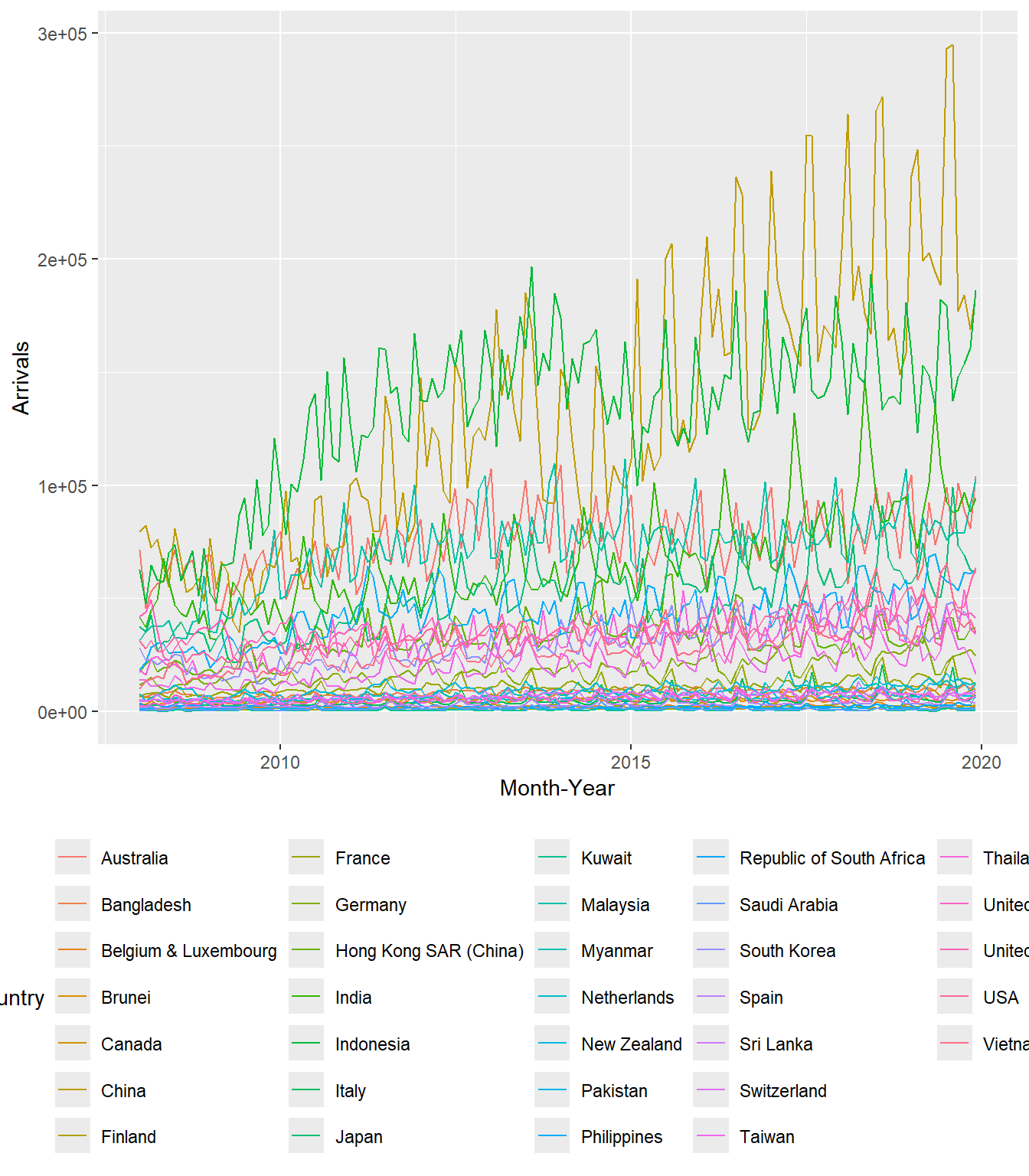

19.3.2 Plotting multiple time-series data with ggplot2 methods

ggplot(data = ts_longer,

aes(x = `Month-Year`,

y = Arrivals,

color = Country))+

geom_line(size = 0.5) +

theme(legend.position = "bottom",

legend.box.spacing = unit(0.5, "cm"))

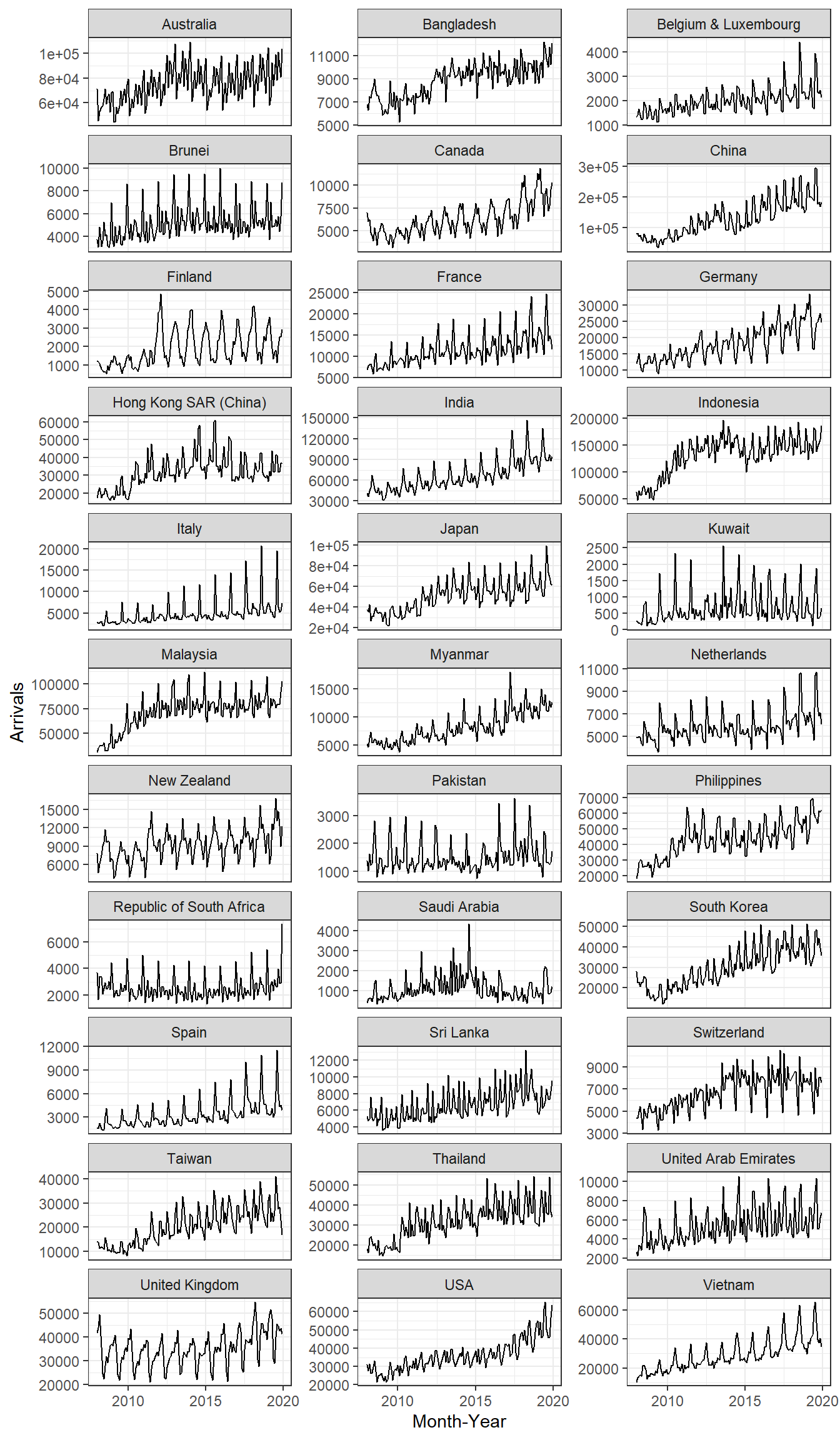

In order to provide effective comparison, facet_wrap() of ggplot2 package is used to create small multiple line graph also known as trellis plot.

ggplot(data = ts_longer,

aes(x = `Month-Year`,

y = Arrivals))+

geom_line(size = 0.5) +

facet_wrap(~ Country,

ncol = 3,

scales = "free_y") +

theme_bw()

19.4 Visual Analysis of Time-series Data

Time series datasets can contain a seasonal component.

This is a cycle that repeats over time, such as monthly or yearly. This repeating cycle may obscure the signal that we wish to model when forecasting, and in turn may provide a strong signal to our predictive models.

In this section, you will discover how to identify seasonality in time series data by using functions provides by feasts packages.

In order to visualise the time-series data effectively, we need to organise the data frame from wide to long format by using pivot_longer() of tidyr package as shown below.

tsibble_longer <- ts_tsibble %>%

pivot_longer(cols = c(2:34),

names_to = "Country",

values_to = "Arrivals")19.4.1 Visual Analysis of Seasonality with Seasonal Plot

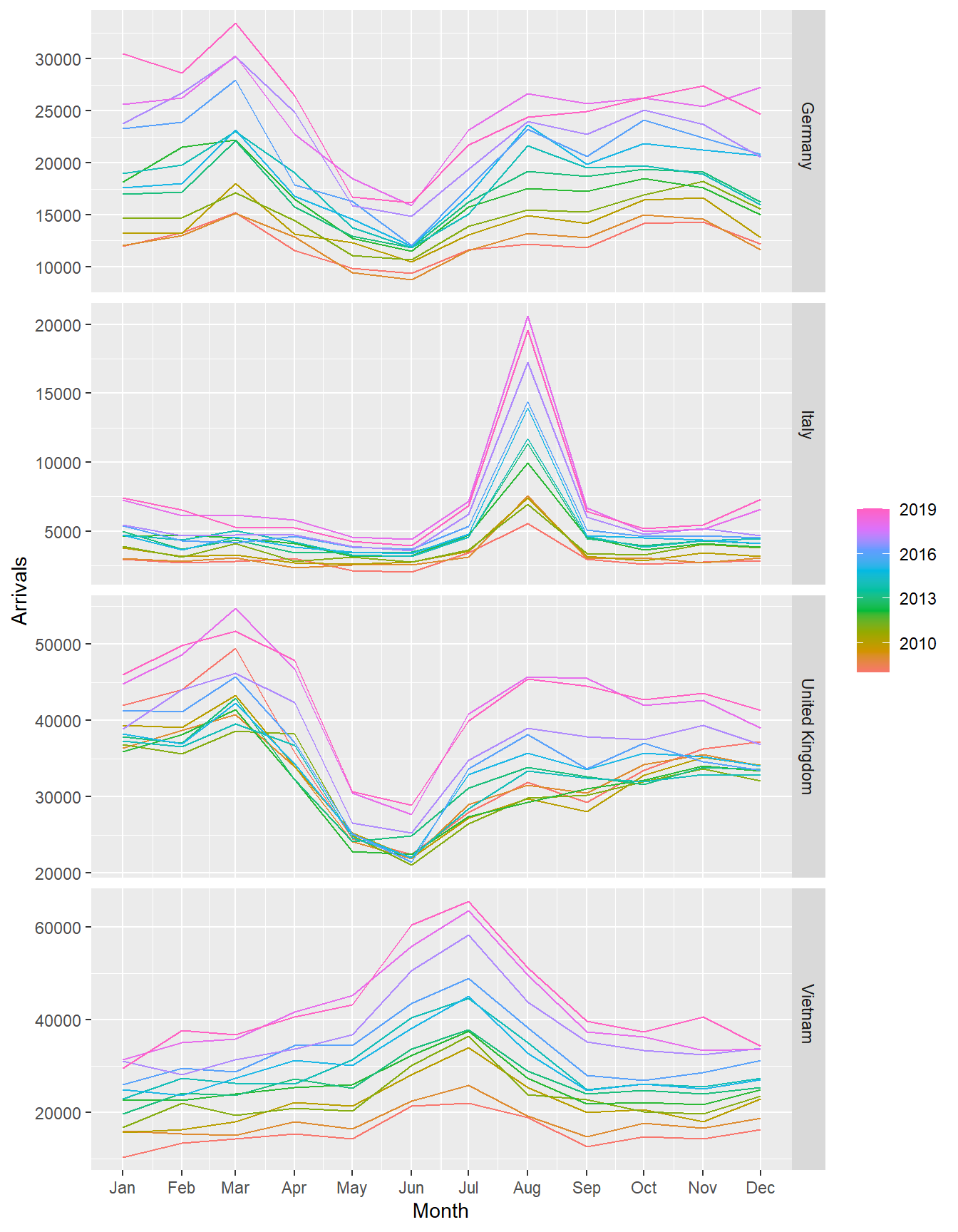

A seasonal plot is similar to a time plot except that the data are plotted against the individual seasons in which the data were observed.

A season plot is created by using gg_season() of feasts package.

tsibble_longer %>%

filter(Country == "Italy" |

Country == "Vietnam" |

Country == "United Kingdom" |

Country == "Germany") %>%

gg_season(Arrivals)

19.4.2 Visual Analysis of Seasonality with Cycle Plot

A cycle plot shows how a trend or cycle changes over time. We can use them to see seasonal patterns. Typically, a cycle plot shows a measure on the Y-axis and then shows a time period (such as months or seasons) along the X-axis. For each time period, there is a trend line across a number of years.

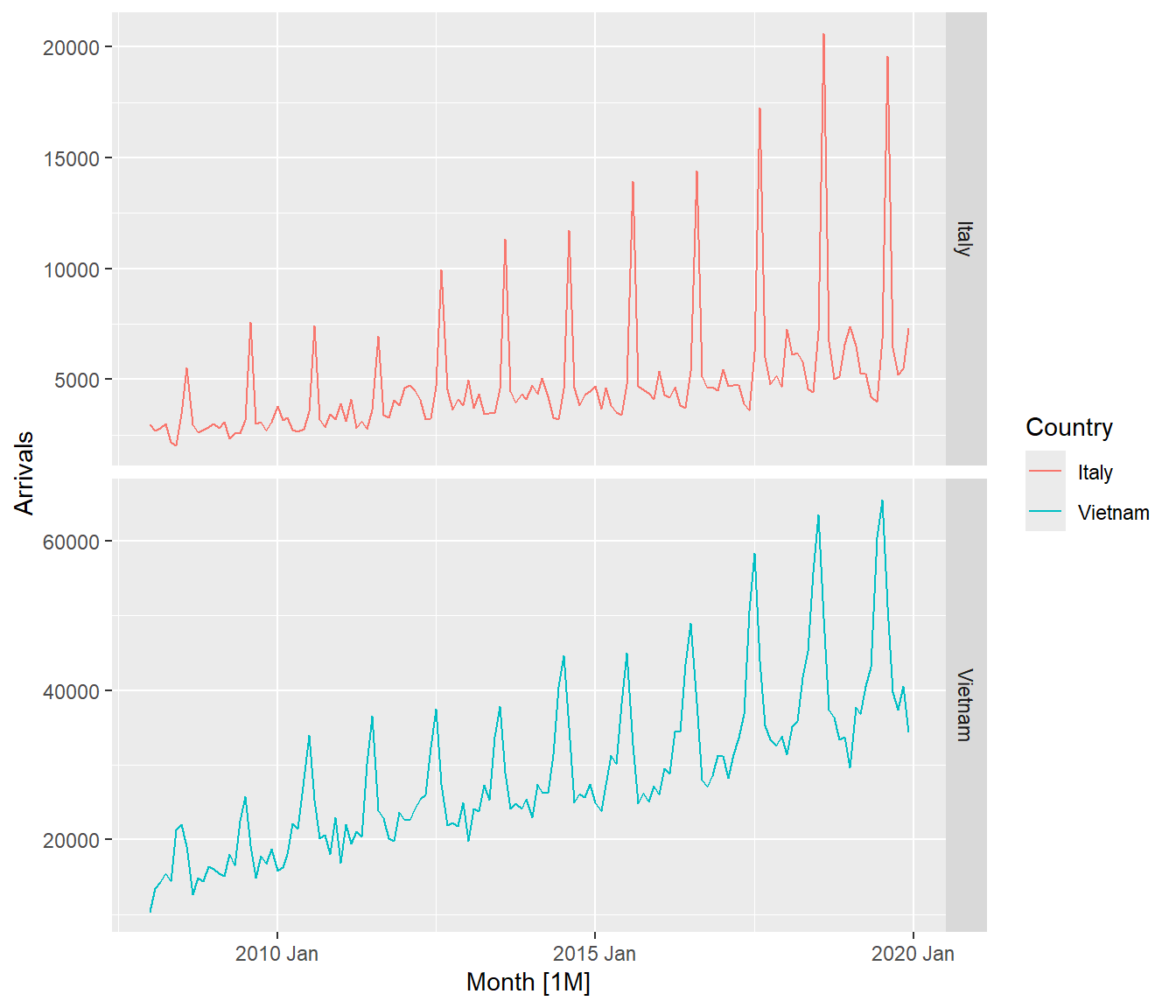

Figure below shows two time-series lines of visitor arrivals from Vietnam and Italy. Both lines reveal clear sign of seasonal patterns but not the trend.

tsibble_longer %>%

filter(Country == "Vietnam" |

Country == "Italy") %>%

autoplot(Arrivals) +

facet_grid(Country ~ ., scales = "free_y")

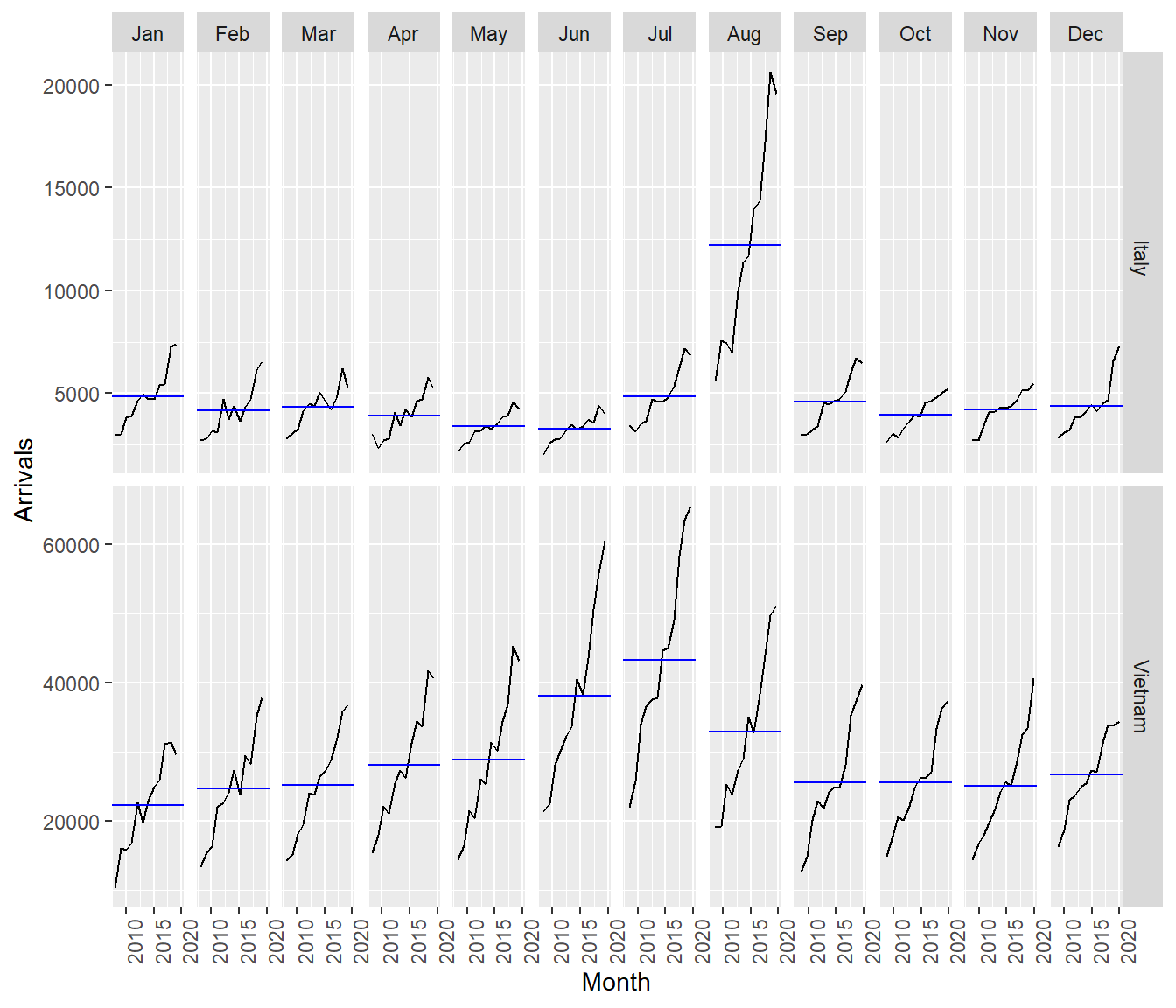

In the code chunk below, cycle plots using gg_subseries() of feasts package are created. Notice that the cycle plots show not only seasonal patterns but also trend.

tsibble_longer %>%

filter(Country == "Vietnam" |

Country == "Italy") %>%

gg_subseries(Arrivals)

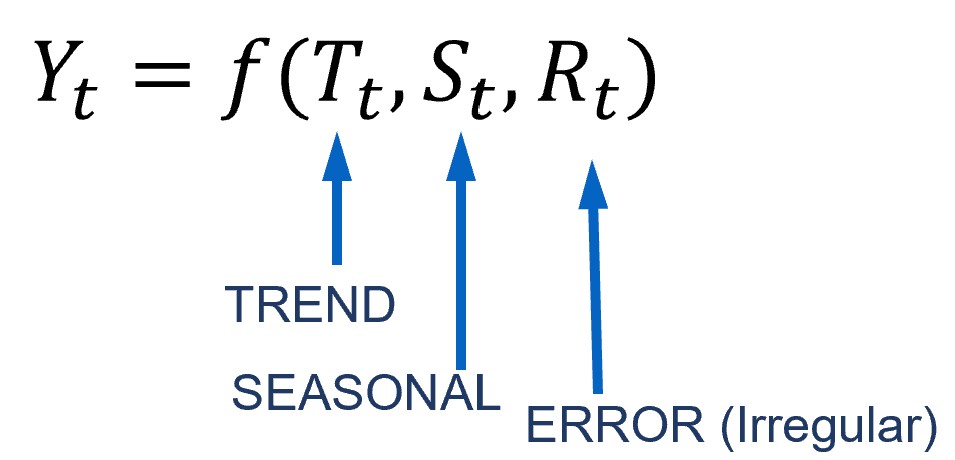

19.5 Time series decomposition

Time series decomposition allows us to isolate structural components such as trend and seasonality from the time-series data.

19.5.1 Single time series decomposition

In feasts package, time series decomposition is supported by ACF(), PACF(), CCF(), feat_acf(), and feat_pacf(). The output can then be plotted by using autoplot() of feasts package.

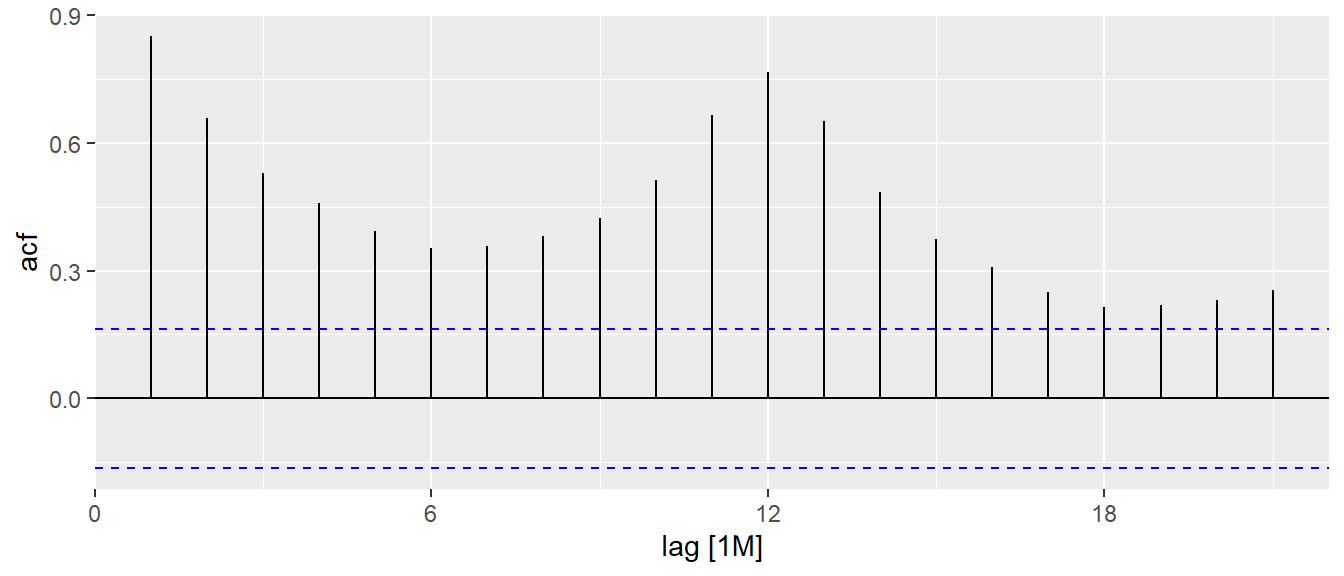

In the code chunk below, ACF() of feasts package is used to plot the ACF curve of visitor arrival from Vietnam.

tsibble_longer %>%

filter(`Country` == "Vietnam") %>%

ACF(Arrivals) %>%

autoplot()

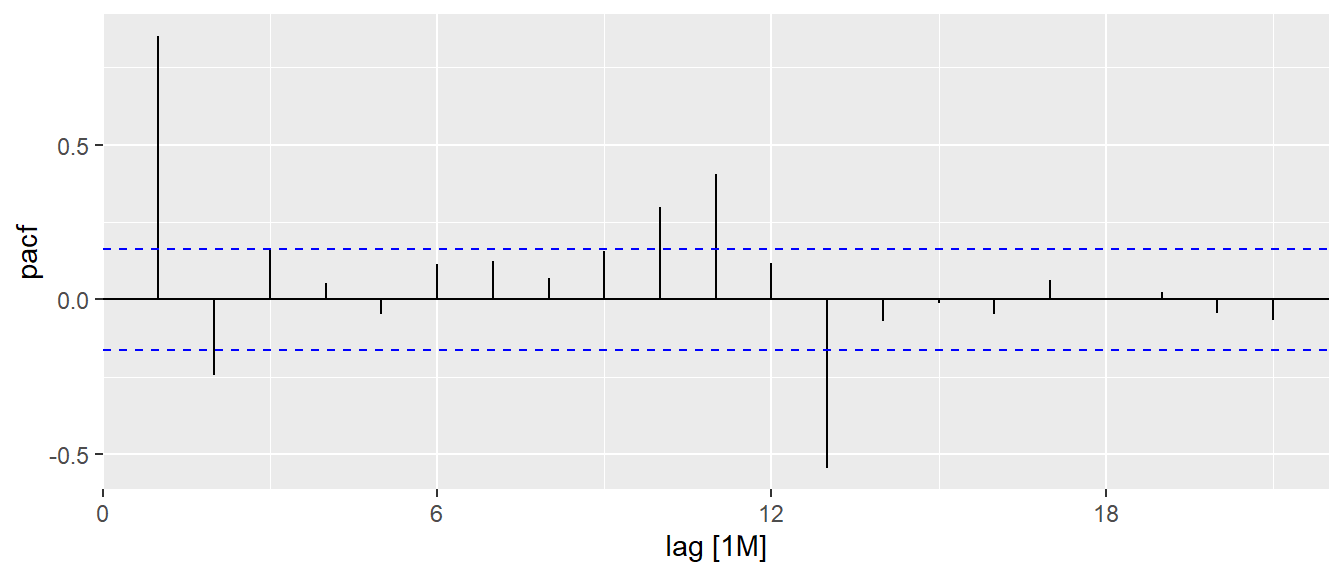

In the code chunk below, PACF() of feasts package is used to plot the Partial ACF curve of visitor arrival from Vietnam.

tsibble_longer %>%

filter(`Country` == "Vietnam") %>%

PACF(Arrivals) %>%

autoplot()

19.5.2 Multiple time-series decomposition

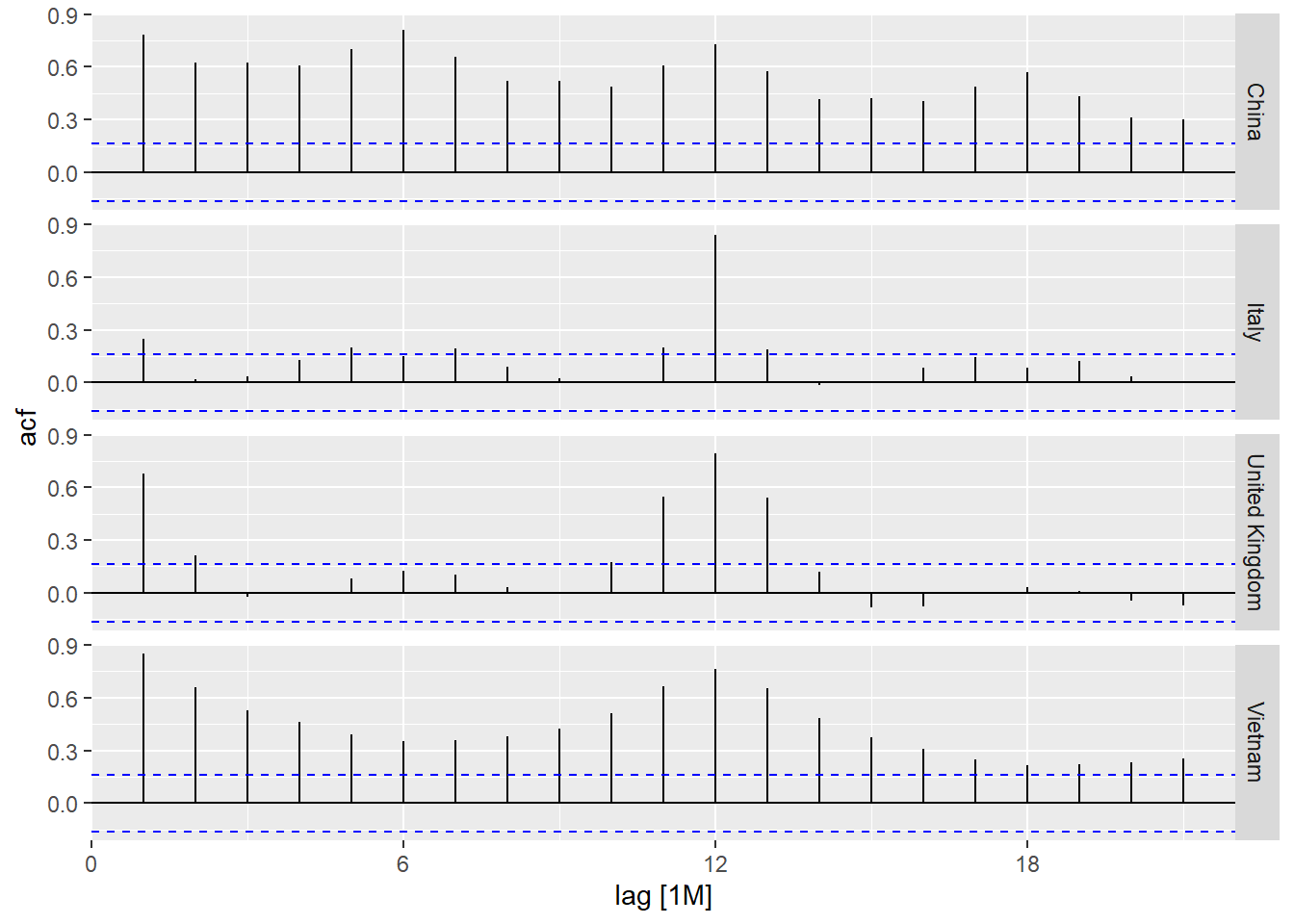

Code chunk below is used to prepare a trellis plot of ACFs for visitor arrivals from Vietnam, Italy, United Kingdom and China.

tsibble_longer %>%

filter(`Country` == "Vietnam" |

`Country` == "Italy" |

`Country` == "United Kingdom" |

`Country` == "China") %>%

ACF(Arrivals) %>%

autoplot()

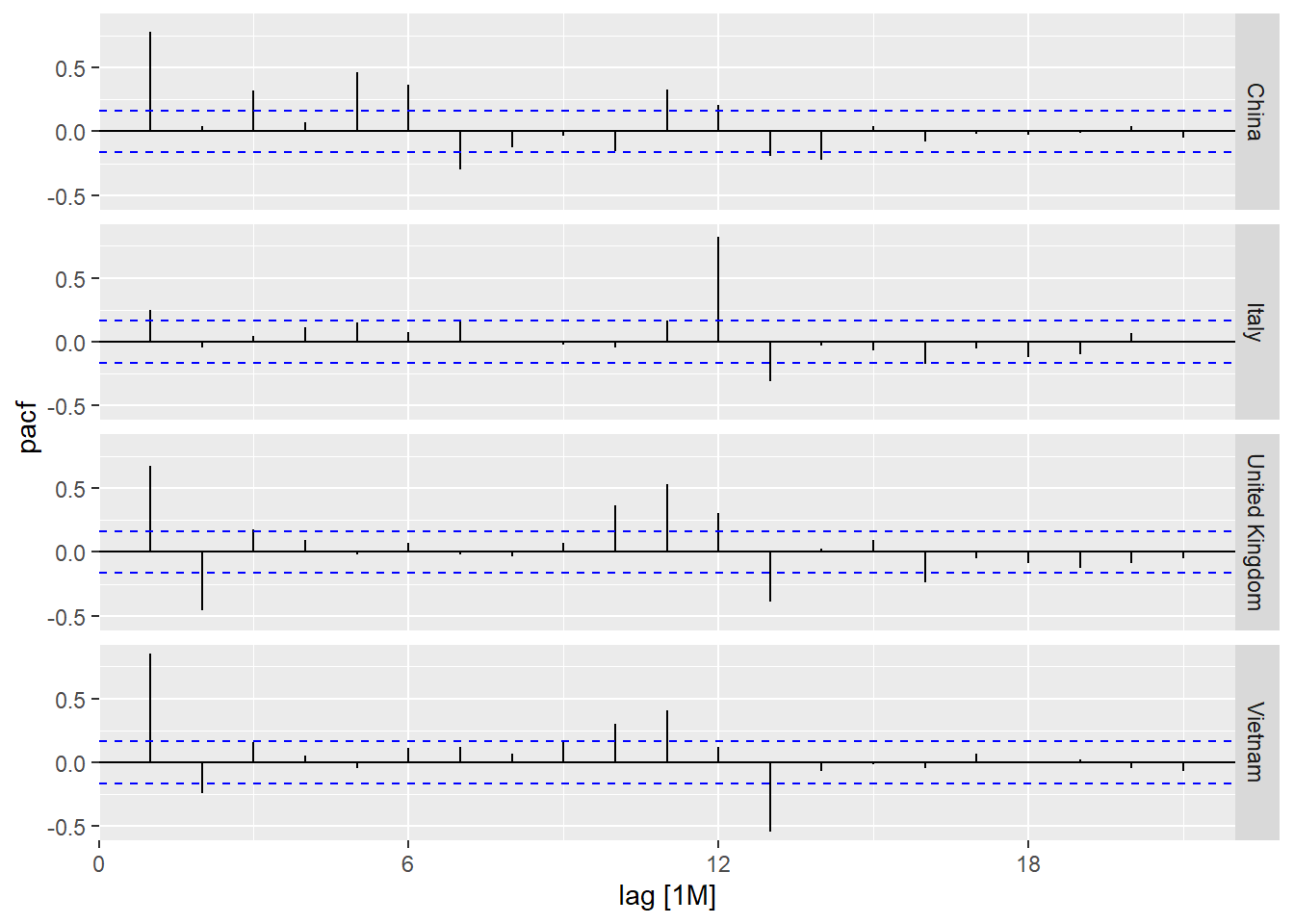

On the other hand, code chunk below is used to prepare a trellis plot of PACFs for visitor arrivals from Vietnam, Italy, United Kingdom and China.

tsibble_longer %>%

filter(`Country` == "Vietnam" |

`Country` == "Italy" |

`Country` == "United Kingdom" |

`Country` == "China") %>%

PACF(Arrivals) %>%

autoplot()

19.5.3 Composite plot of time series decomposition

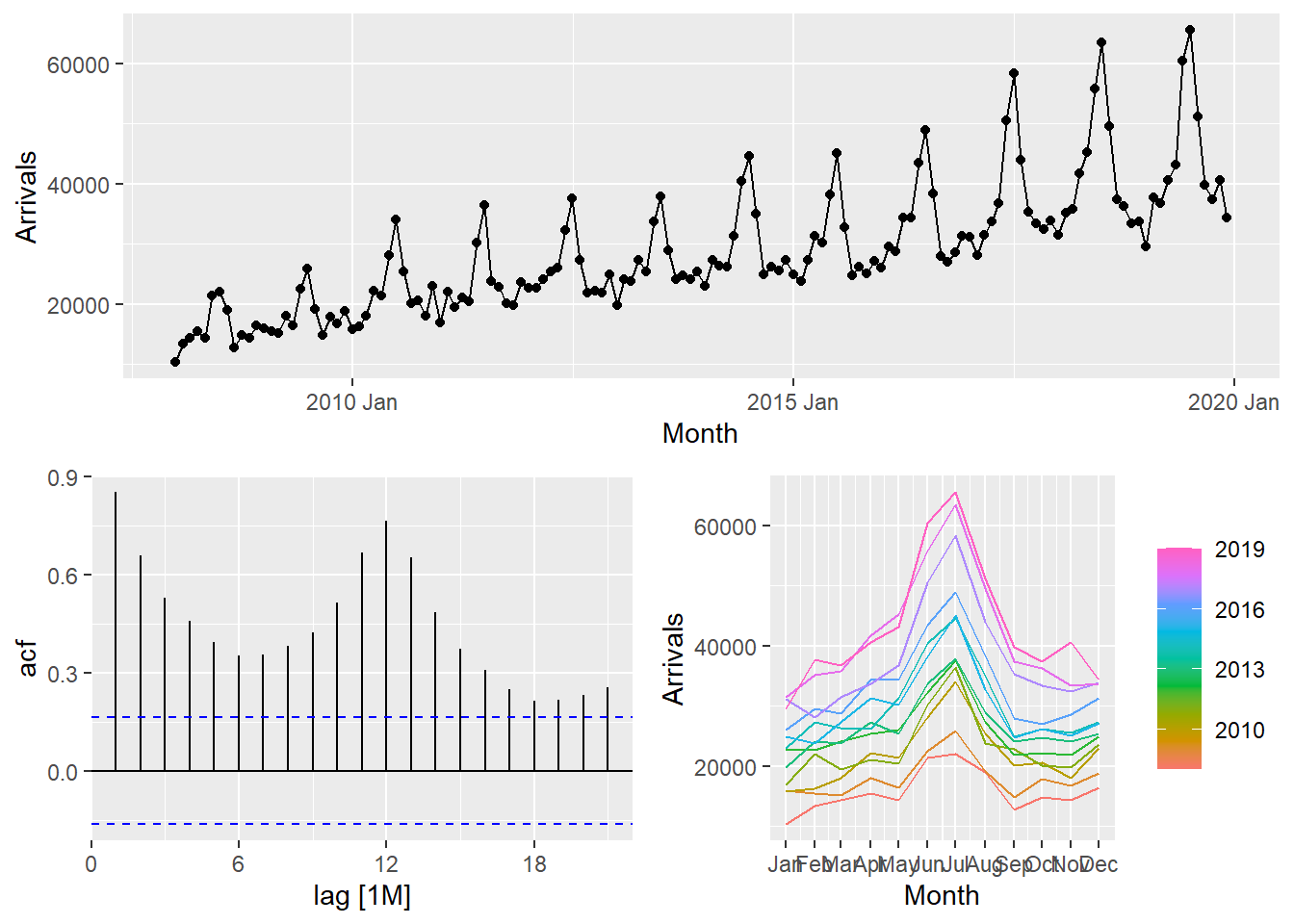

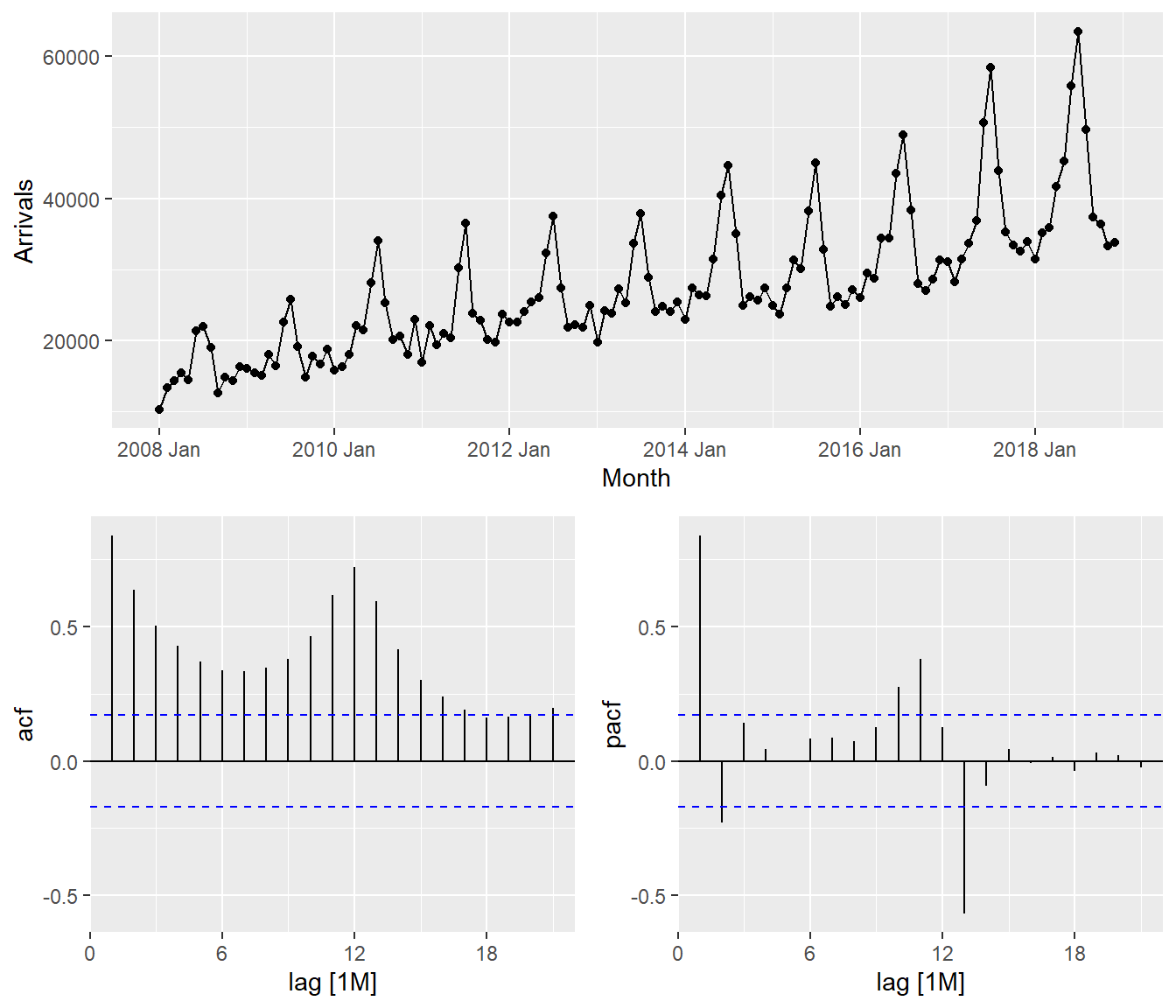

One of the interesting function of feasts package time series decomposition is gg_tsdisplay(). It provides a composite plot by showing the original line graph on the top pane follow by the ACF on the left and seasonal plot on the right.

tsibble_longer %>%

filter(`Country` == "Vietnam") %>%

gg_tsdisplay(Arrivals)

19.6 Visual STL Diagnostics

STL is an acronym for “Seasonal and Trend decomposition using Loess”, while Loess is a method for estimating nonlinear relationships. It was developed by R. B. Cleveland, Cleveland, McRae, & Terpenning (1990).

STL is a robust method of time series decomposition often used in economic and environmental analyses. The STL method uses locally fitted regression models to decompose a time series into trend, seasonal, and remainder components.

The STL algorithm performs smoothing on the time series using LOESS in two loops; the inner loop iterates between seasonal and trend smoothing and the outer loop minimizes the effect of outliers. During the inner loop, the seasonal component is calculated first and removed to calculate the trend component. The remainder is calculated by subtracting the seasonal and trend components from the time series.

STL has several advantages over the classical, SEATS and X11 decomposition methods:

- Unlike SEATS and X11, STL will handle any type of seasonality, not only monthly and quarterly data.

- The seasonal component is allowed to change over time, and the rate of change can be controlled by the user.

- The smoothness of the trend-cycle can also be controlled by the user.

- It can be robust to outliers (i.e., the user can specify a robust decomposition), so that occasional unusual observations will not affect the estimates of the trend-cycle and seasonal components. They will, however, affect the remainder component.

19.6.1 Visual STL diagnostics with feasts

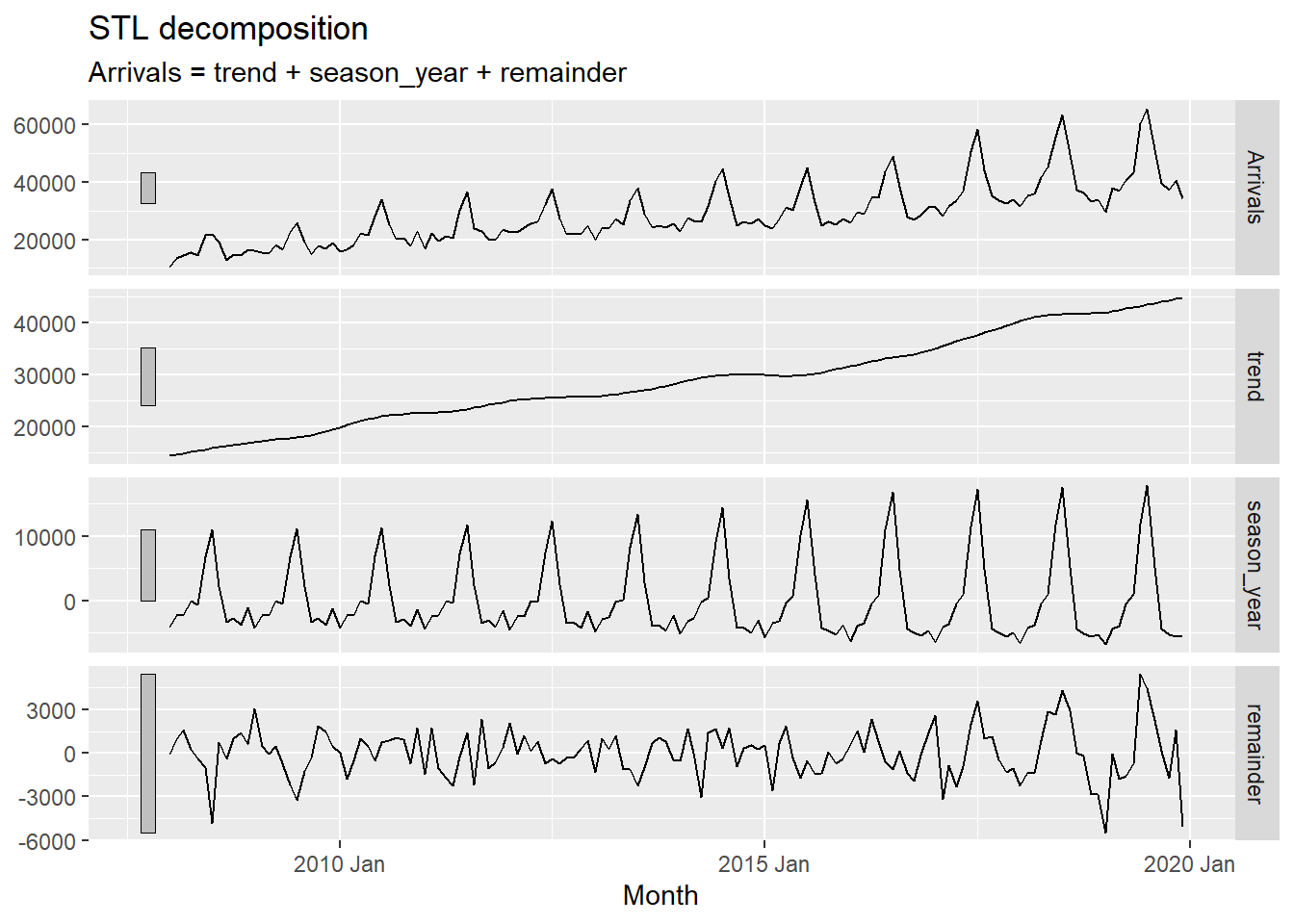

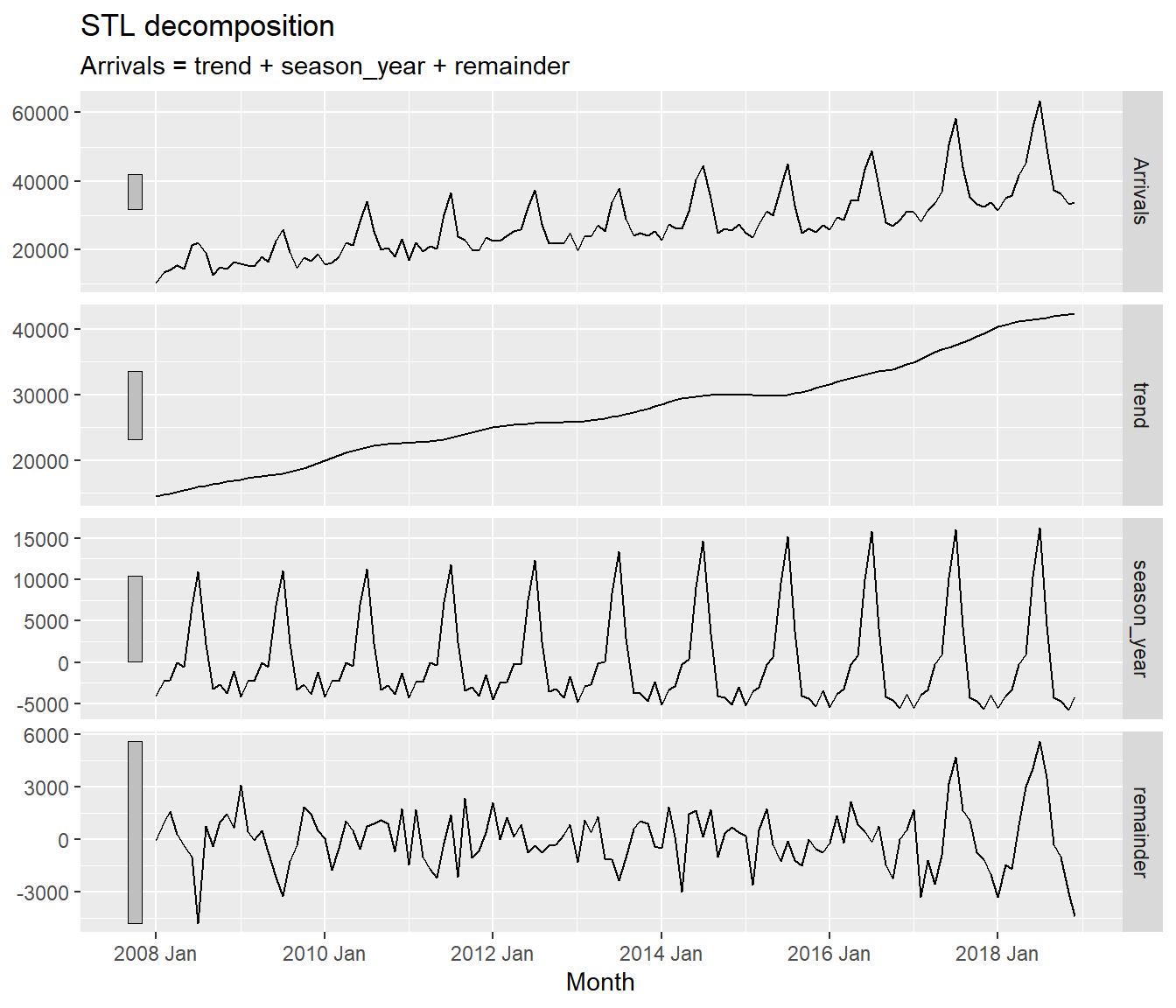

In the code chunk below, STL() of feasts package is used to decomposite visitor arrivals from Vietnam data.

tsibble_longer %>%

filter(`Country` == "Vietnam") %>%

model(stl = STL(Arrivals)) %>%

components() %>%

autoplot()

The grey bars to the left of each panel show the relative scales of the components. Each grey bar represents the same length but because the plots are on different scales, the bars vary in size. The large grey bar in the bottom panel shows that the variation in the remainder component is smallest compared to the variation in the data. If we shrank the bottom three panels until their bars became the same size as that in the data panel, then all the panels would be on the same scale.

19.6.2 Classical Decomposition with feasts

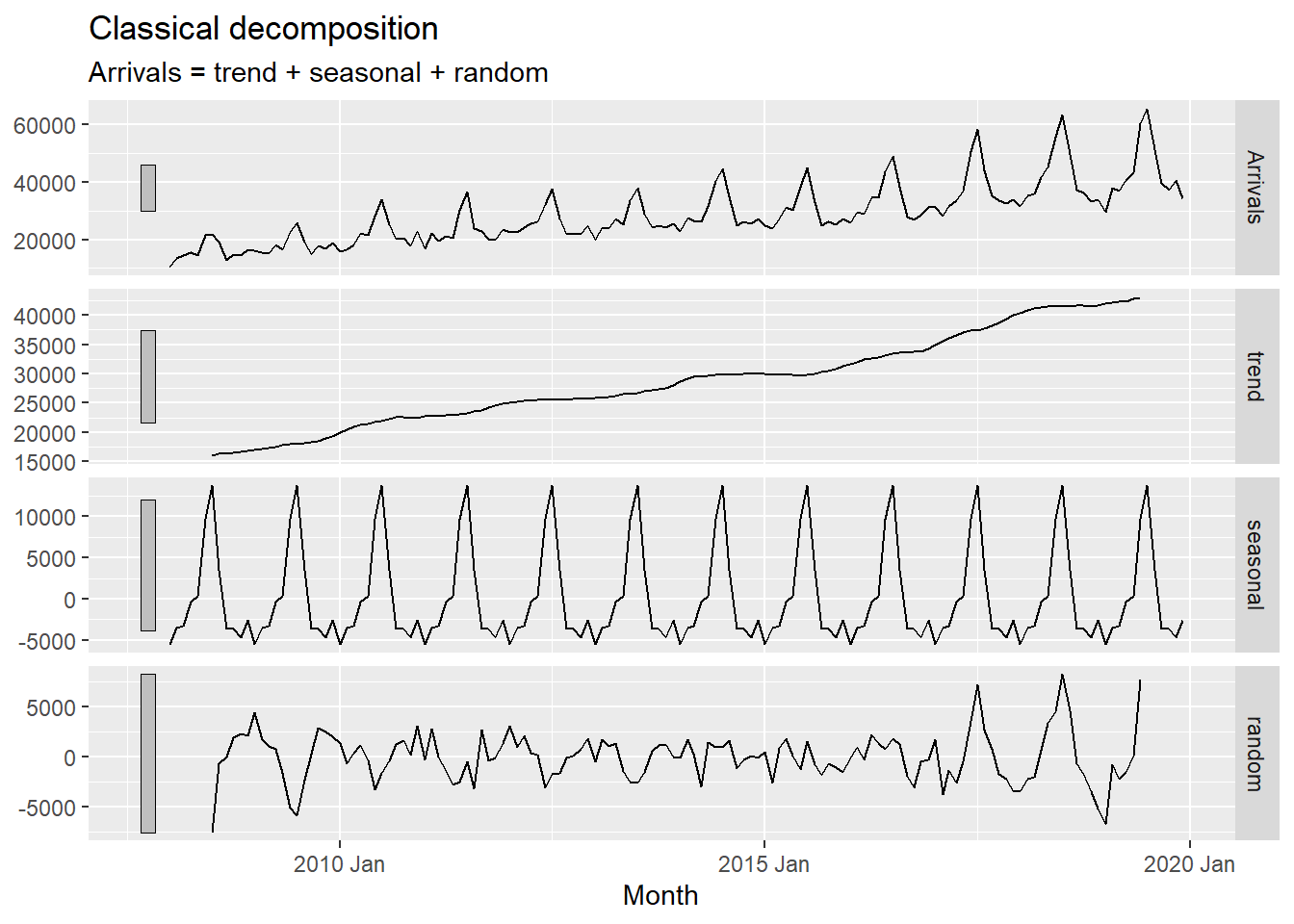

In the code chunk below, classical_decomposition() of feasts package is used to decompose a time series into seasonal, trend and irregular components using moving averages. THe function is able to deal with both additive or multiplicative seasonal component.

tsibble_longer %>%

filter(`Country` == "Vietnam") %>%

model(

classical_decomposition(

Arrivals, type = "additive")) %>%

components() %>%

autoplot()

19.7 Visual Forecasting

In this section, two R packages belong to tidyverts family will be used they are:

fable provides a collection of commonly used univariate and multivariate time series forecasting models including exponential smoothing via state space models and automatic ARIMA modelling. It is a tidy version of the popular forecast package and a member of tidyverts.

fabletools provides tools for building modelling packages, with a focus on time series forecasting. This package allows package developers to extend fable with additional models, without needing to depend on the models supported by fable.

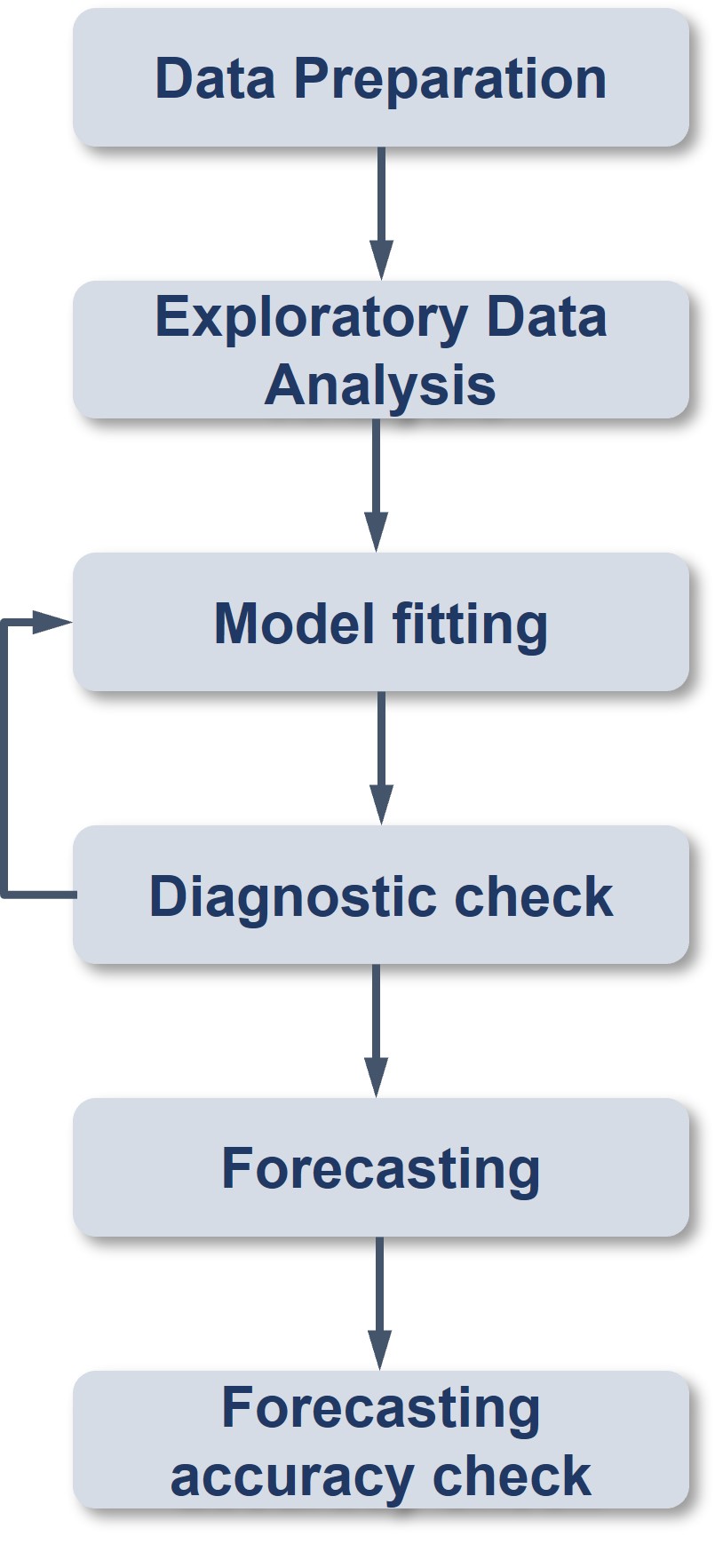

Figure below shows a typical flow of a time-series forecasting process.

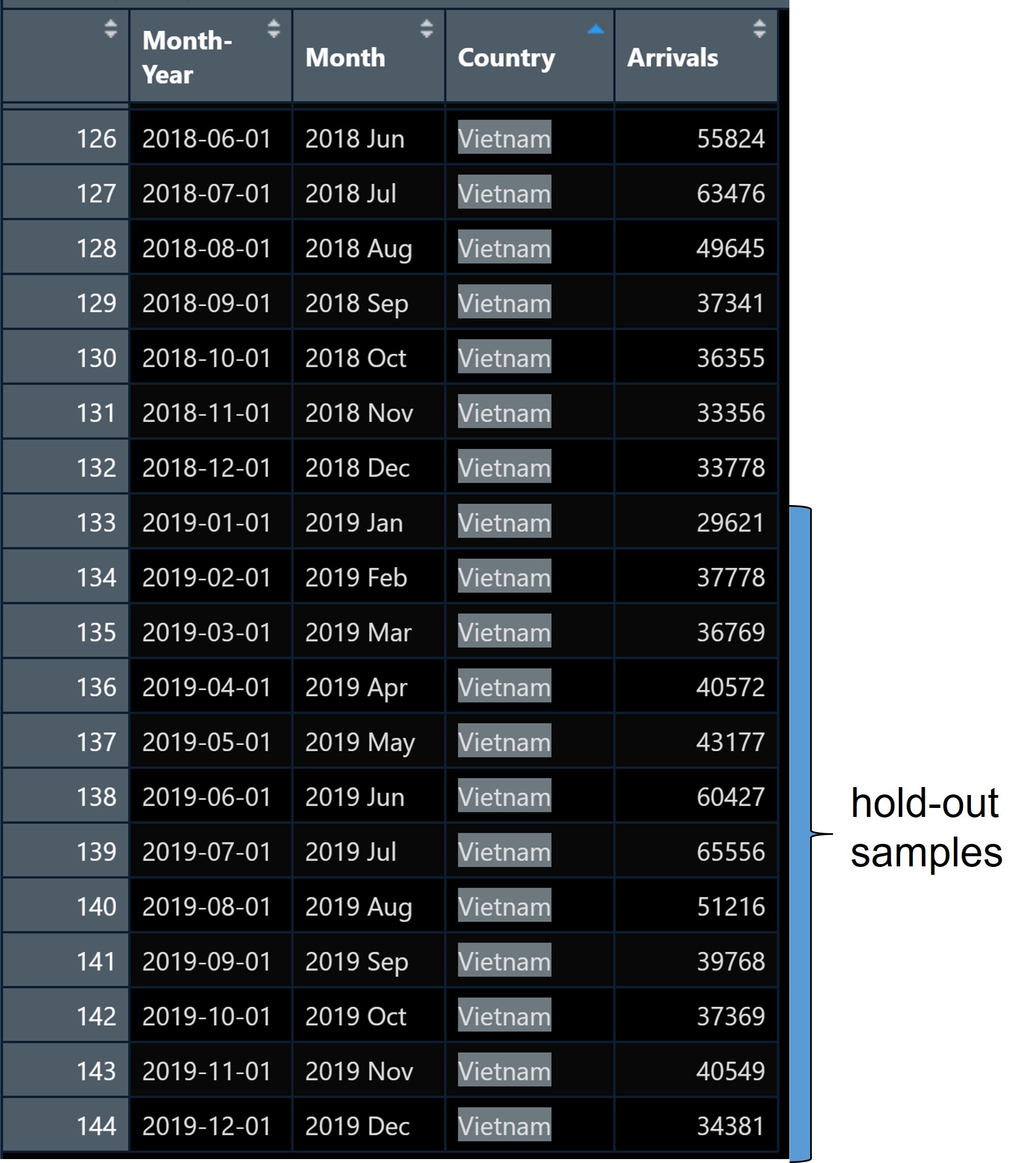

19.7.1 Time Series Data Sampling

A good practice in forecasting is to split the original data set into a training and a hold-out data sets. The first part is called estimate sample (also known as training data). It will be used to estimate the starting values and the smoothing parameters. This sample typically contains 75-80 percent of the observation, although the forecaster may choose to use a smaller percentage for longer series.

The second part of the time series is called hold-out sample. It is used to check the forecasting performance. No matter how many parameters are estimated with the estimation sample, each method under consideration can be evaluated with the use of the “new” observation contained in the hold-out sample.

In this example we will use the last 12 months for hold-out and the rest for training.

First, an extra column called Type indicating training or hold-out will be created by using mutate() of dplyr package. It will be extremely useful for subsequent data visualisation.

vietnam_ts <- tsibble_longer %>%

filter(Country == "Vietnam") %>%

mutate(Type = if_else(

`Month-Year` >= "2019-01-01",

"Hold-out", "Training"))Next, a training data set is extracted from the original data set by using filter() of dplyr package.

vietnam_train <- vietnam_ts %>%

filter(`Month-Year` < "2019-01-01")19.7.2 Exploratory Data Analysis (EDA): Time Series Data

Before fitting forecasting models, it is a good practice to analysis the time series data by using EDA methods.

vietnam_train %>%

model(stl = STL(Arrivals)) %>%

components() %>%

autoplot()

19.7.3 Fitting forecasting models

19.7.3.1 Fitting Exponential Smoothing State Space (ETS) Models: fable methods

In fable, Exponential Smoothing State Space Models are supported by ETS(). The combinations are specified through the formula:

ETS(y ~ error(c("A", "M"))

+ trend(c("N", "A", "Ad"))

+ season(c("N", "A", "M"))19.7.3.2 Fitting a simple exponential smoothing (SES)

.pull-left[

fit_ses <- vietnam_train %>%

model(ETS(Arrivals ~ error("A")

+ trend("N")

+ season("N")))

fit_ses# A mable: 1 x 2

# Key: Country [1]

Country `ETS(Arrivals ~ error("A") + trend("N") + season("N"))`

<chr> <model>

1 Vietnam <ETS(A,N,N)>Notice that model() of fable package is used to estimate the ETS model on a particular dataset, and returns a mable (model table) object.

A mable contains a row for each time series (uniquely identified by the key variables), and a column for each model specification. A model is contained within the cells of each model column.

19.7.3.3 Examine Model Assumptions

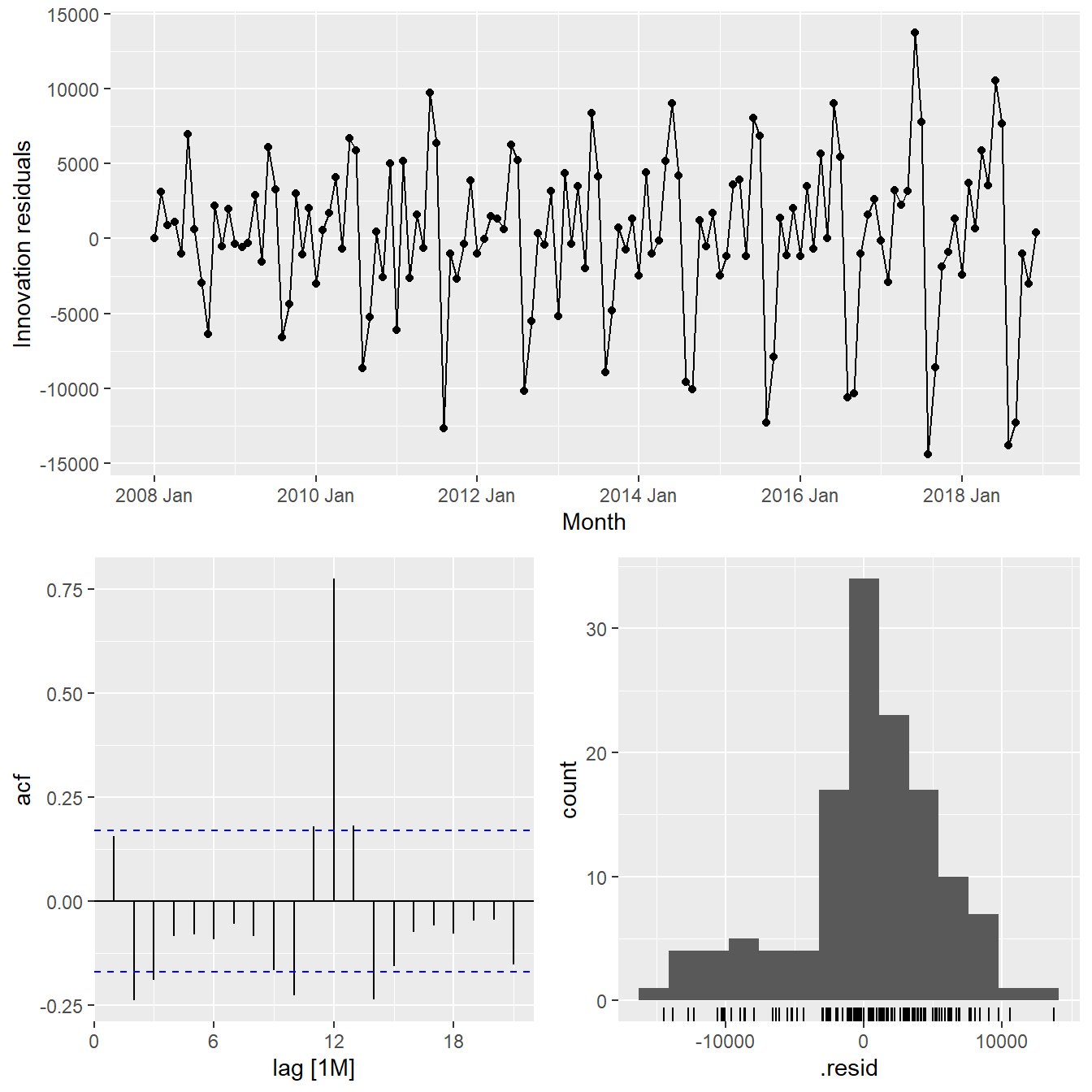

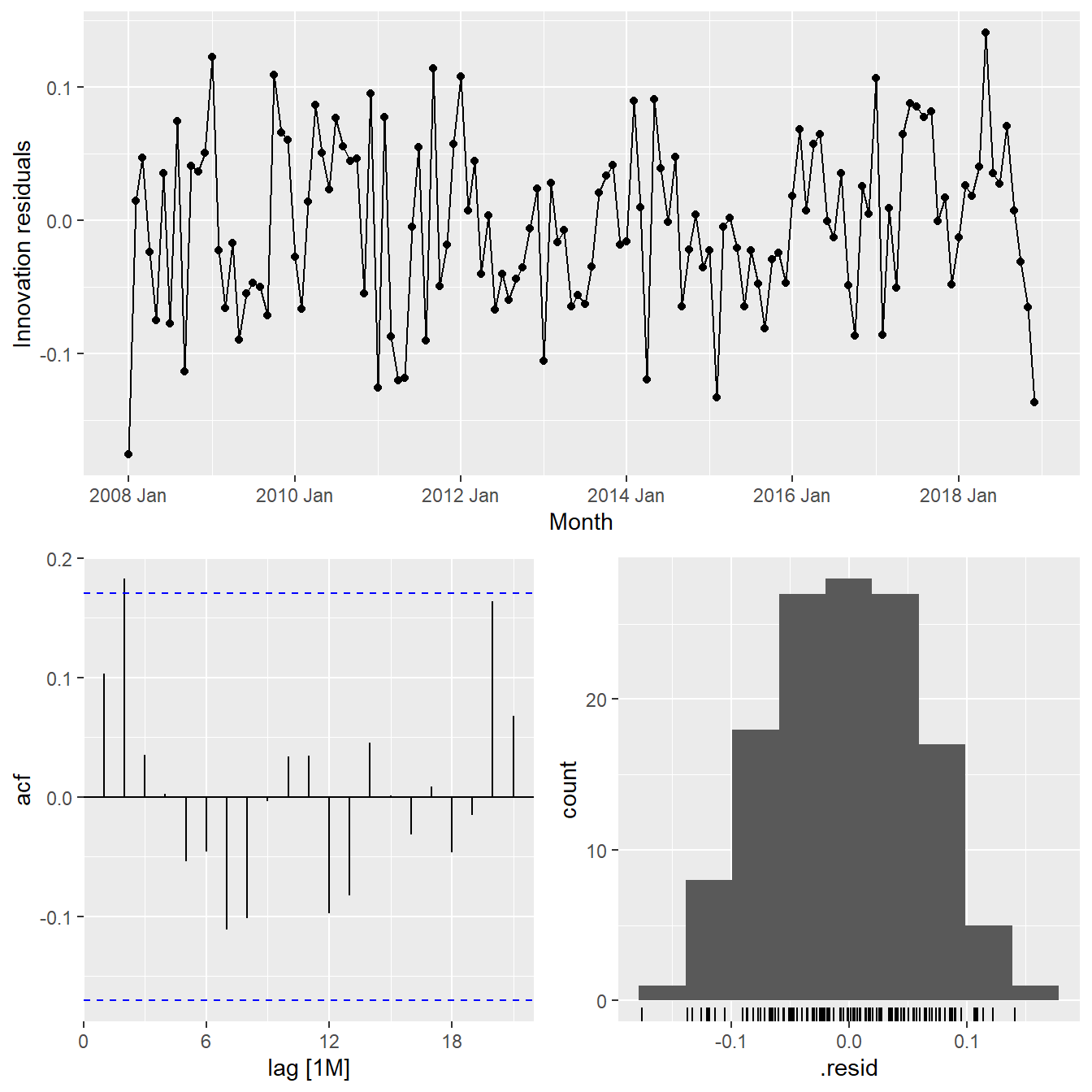

Next, gg_tsresiduals() of feasts package is used to check the model assumptions with residuals plots.

gg_tsresiduals(fit_ses)

19.7.3.4 The model details

report() of fabletools is be used to reveal the model details.

fit_ses %>%

report()Series: Arrivals

Model: ETS(A,N,N)

Smoothing parameters:

alpha = 0.9998995

Initial states:

l[0]

10312.99

sigma^2: 27939164

AIC AICc BIC

2911.726 2911.913 2920.374 19.7.3.5 Fitting ETS Methods with Trend: Holt’s Linear

19.7.3.6 Trend methods

vietnam_H <- vietnam_train %>%

model(`Holt's method` =

ETS(Arrivals ~ error("A") +

trend("A") +

season("N")))

vietnam_H %>% report()Series: Arrivals

Model: ETS(A,A,N)

Smoothing parameters:

alpha = 0.9998995

beta = 0.0001004625

Initial states:

l[0] b[0]

13673.29 525.8859

sigma^2: 28584805

AIC AICc BIC

2916.695 2917.171 2931.109 19.7.3.7 Damped Trend methods

vietnam_HAd <- vietnam_train %>%

model(`Holt's method` =

ETS(Arrivals ~ error("A") +

trend("Ad") +

season("N")))

vietnam_HAd %>% report()Series: Arrivals

Model: ETS(A,Ad,N)

Smoothing parameters:

alpha = 0.9998999

beta = 0.0001098602

phi = 0.9784562

Initial states:

l[0] b[0]

13257.28 523.54

sigma^2: 28641536

AIC AICc BIC

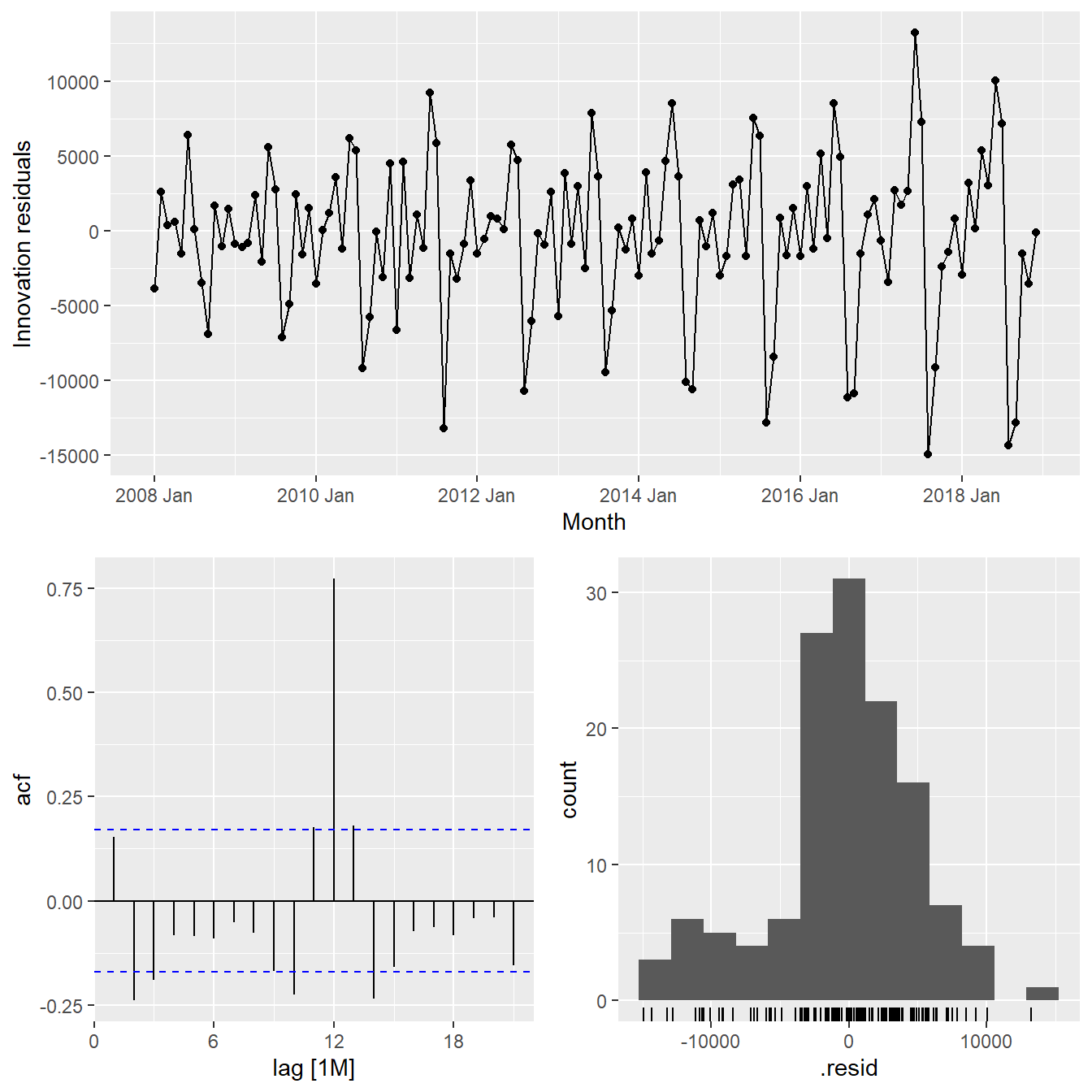

2917.921 2918.593 2935.218 19.7.3.8 Checking for results

Check the model assumptions with residuals plots.

gg_tsresiduals(vietnam_H)

gg_tsresiduals(vietnam_HAd)

19.7.4 Fitting ETS Methods with Season: Holt-Winters

Vietnam_WH <- vietnam_train %>%

model(

Additive = ETS(Arrivals ~ error("A")

+ trend("A")

+ season("A")),

Multiplicative = ETS(Arrivals ~ error("M")

+ trend("A")

+ season("M"))

)

Vietnam_WH %>% report()# A tibble: 2 × 10

Country .model sigma2 log_lik AIC AICc BIC MSE AMSE MAE

<chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 Vietnam Additive 5.33e+6 -1336. 2706. 2711. 2755. 4.68e6 8.56e6 1.72e+3

2 Vietnam Multiplicative 4.55e-3 -1300. 2635. 2640. 2684. 3.05e6 3.42e6 5.20e-219.7.5 Fitting multiple ETS Models

fit_ETS <- vietnam_train %>%

model(`SES` = ETS(Arrivals ~ error("A") +

trend("N") +

season("N")),

`Holt`= ETS(Arrivals ~ error("A") +

trend("A") +

season("N")),

`damped Holt` =

ETS(Arrivals ~ error("A") +

trend("Ad") +

season("N")),

`WH_A` = ETS(

Arrivals ~ error("A") +

trend("A") +

season("A")),

`WH_M` = ETS(Arrivals ~ error("M")

+ trend("A")

+ season("M"))

)19.7.6 The model coefficient

tidy() of fabletools is be used to extract model coefficients from a mable.

fit_ETS %>%

tidy()# A tibble: 45 × 4

Country .model term estimate

<chr> <chr> <chr> <dbl>

1 Vietnam SES alpha 1.00

2 Vietnam SES l[0] 10313.

3 Vietnam Holt alpha 1.00

4 Vietnam Holt beta 0.000100

5 Vietnam Holt l[0] 13673.

6 Vietnam Holt b[0] 526.

7 Vietnam damped Holt alpha 1.00

8 Vietnam damped Holt beta 0.000110

9 Vietnam damped Holt phi 0.978

10 Vietnam damped Holt l[0] 13257.

# ℹ 35 more rows19.7.7 Step 4: Model Comparison

glance() of fabletool

fit_ETS %>%

report()# A tibble: 5 × 10

Country .model sigma2 log_lik AIC AICc BIC MSE AMSE MAE

<chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 Vietnam SES 2.79e+7 -1453. 2912. 2912. 2920. 27515844. 5.99e7 3.91e+3

2 Vietnam Holt 2.86e+7 -1453. 2917. 2917. 2931. 27718599. 6.03e7 3.92e+3

3 Vietnam damped Holt 2.86e+7 -1453. 2918. 2919. 2935. 27556629. 5.97e7 3.92e+3

4 Vietnam WH_A 5.33e+6 -1336. 2706. 2711. 2755. 4684271. 8.56e6 1.72e+3

5 Vietnam WH_M 4.55e-3 -1300. 2635. 2640. 2684. 3046059. 3.42e6 5.20e-219.7.8 Step 5: Forecasting future values

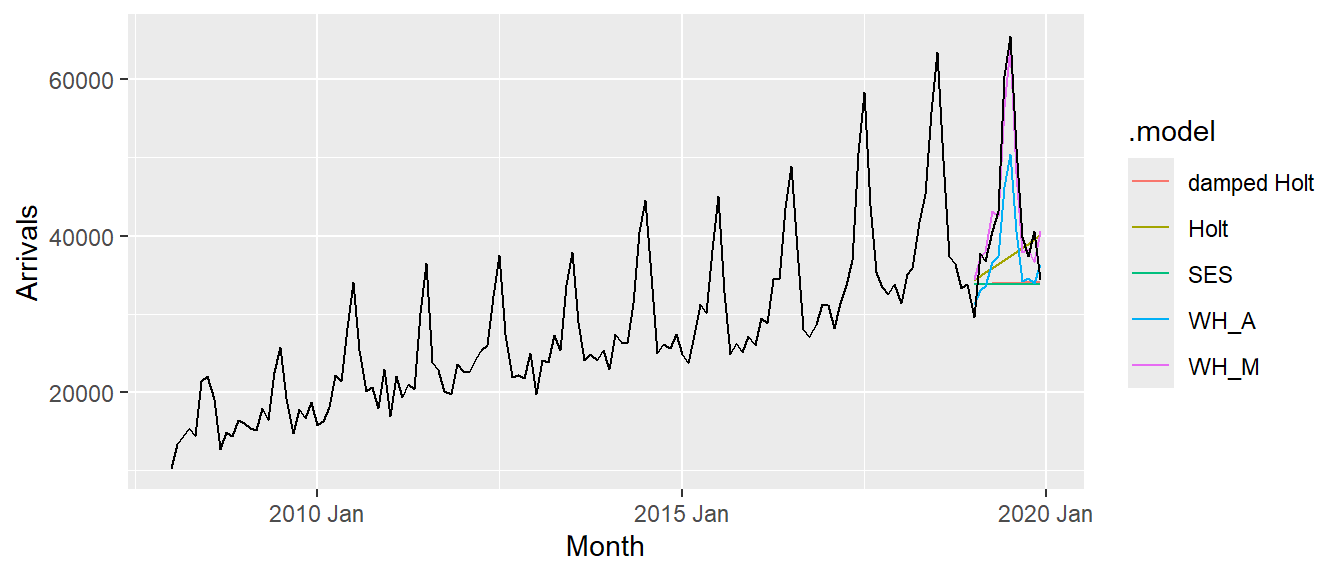

To forecast the future values, forecast() of fable will be used. Notice that the forecast period is 12 months.

fit_ETS %>%

forecast(h = "12 months") %>%

autoplot(vietnam_ts,

level = NULL)

19.7.9 Fitting ETS Automatically

fit_autoETS <- vietnam_train %>%

model(ETS(Arrivals))

fit_autoETS %>% report()Series: Arrivals

Model: ETS(M,A,M)

Smoothing parameters:

alpha = 0.1613503

beta = 0.0001021811

gamma = 0.0001030996

Initial states:

l[0] b[0] s[0] s[-1] s[-2] s[-3] s[-4] s[-5]

15001.12 212.3552 0.9167302 0.8311728 0.8739287 0.8690543 1.104668 1.485584

s[-6] s[-7] s[-8] s[-9] s[-10] s[-11]

1.311207 0.9917759 1.014187 0.8973028 0.8816768 0.8227129

sigma^2: 0.0046

AIC AICc BIC

2634.751 2640.119 2683.759 19.7.10 Fitting Fitting ETS Automatically

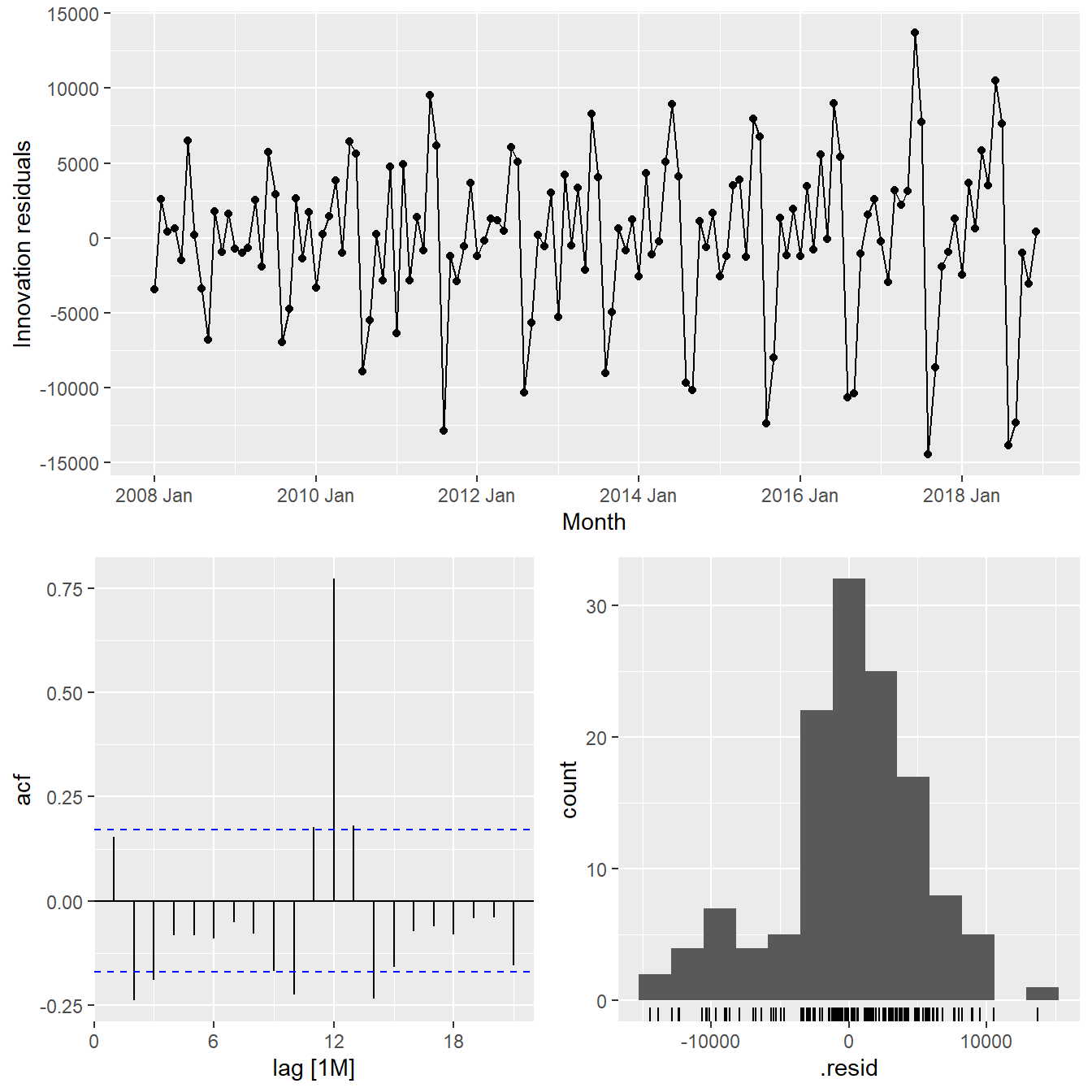

Next, we will check the model assumptions with residuals plots by using gg_tsresiduals() of feasts package

gg_tsresiduals(fit_autoETS)

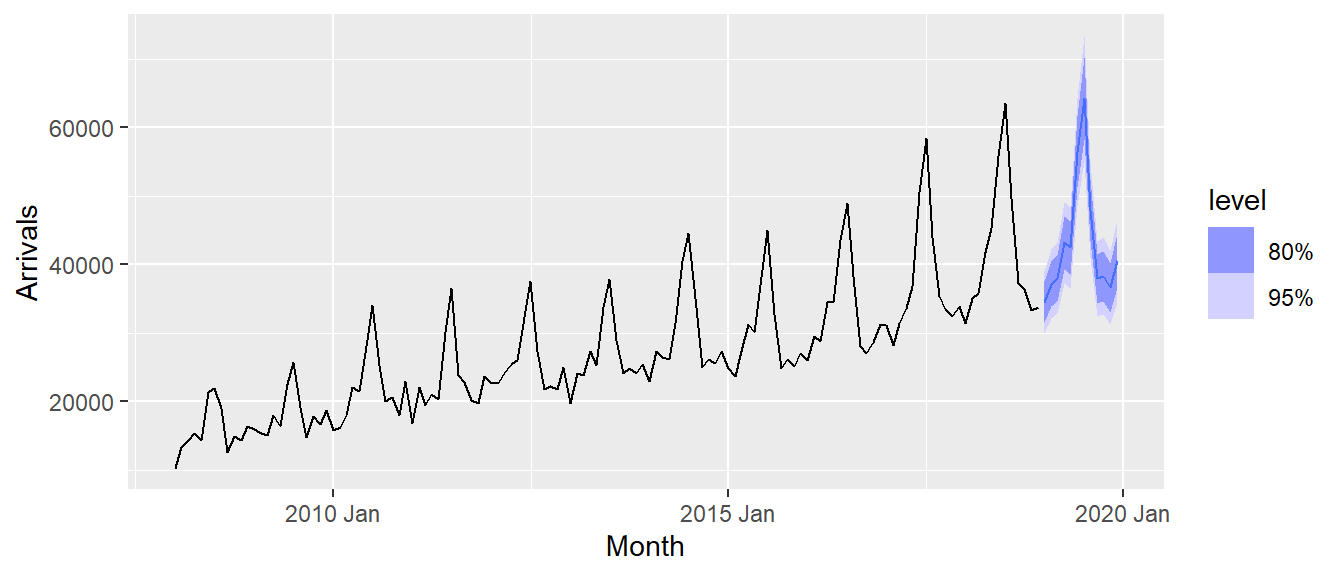

19.7.11 Forecast the future values

In the code chunk below, forecast() of fable package is used to forecast the future values. Then, autoplot() of feasts package is used to see the training data along with the forecast values.

fit_autoETS %>%

forecast(h = "12 months") %>%

autoplot(vietnam_train)

19.7.12 Visualising AutoETS model with ggplot2

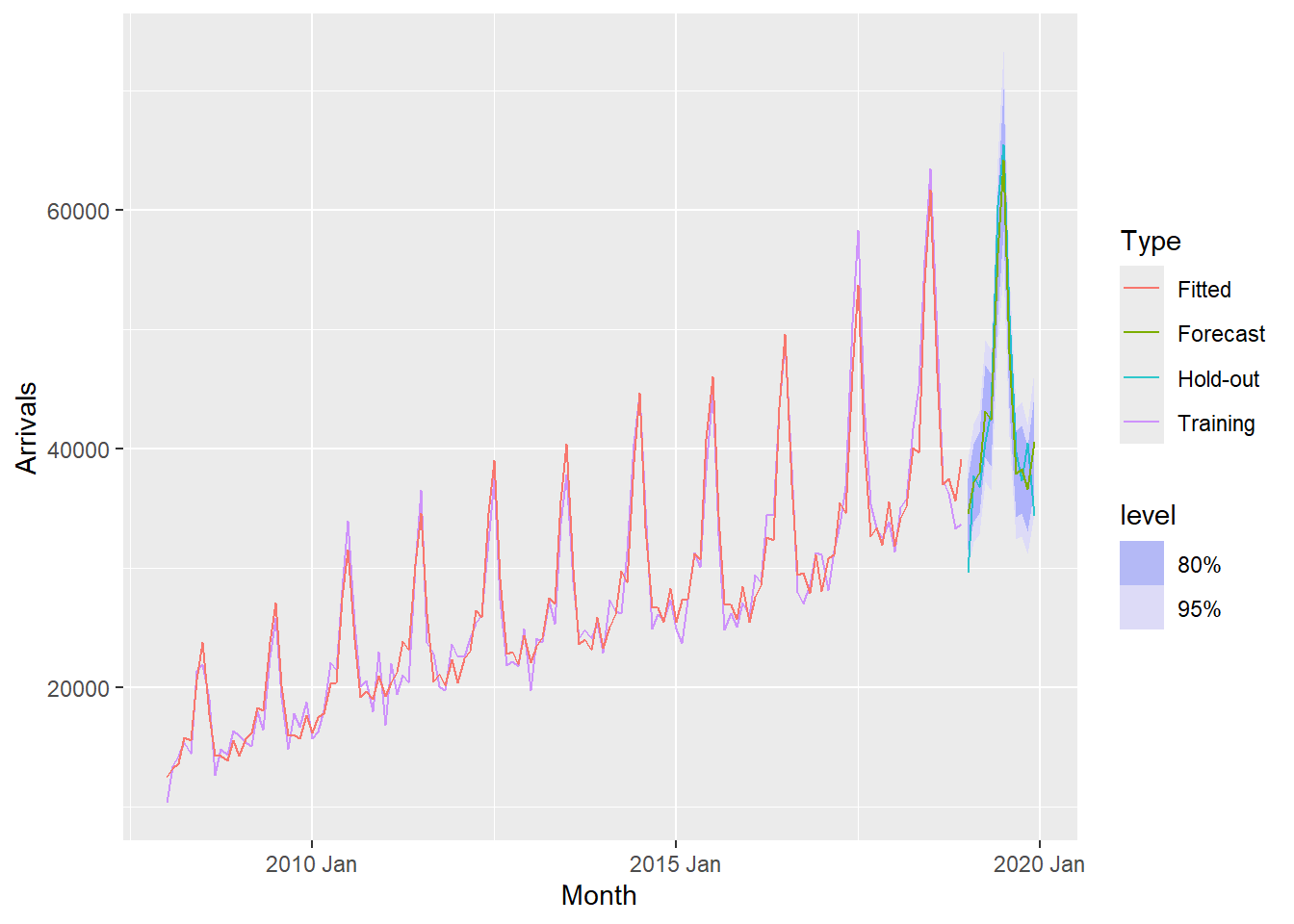

There are time that we are interested to visualise relationship between training data and fit data and forecasted values versus the hold-out data.

19.7.13 Visualising AutoETS model with ggplot2

Code chunk below is used to create the data visualisation in previous slide.

fc_autoETS <- fit_autoETS %>%

forecast(h = "12 months")

vietnam_ts %>%

ggplot(aes(x=`Month`,

y=Arrivals)) +

autolayer(fc_autoETS,

alpha = 0.6) +

geom_line(aes(

color = Type),

alpha = 0.8) +

geom_line(aes(

y = .mean,

colour = "Forecast"),

data = fc_autoETS) +

geom_line(aes(

y = .fitted,

colour = "Fitted"),

data = augment(fit_autoETS))19.8 AutoRegressive Integrated Moving Average(ARIMA) Methods for Time Series Forecasting: fable (tidyverts) methods

19.8.1 Visualising Autocorrelations: feasts methods

feasts package provides a very handy function for visualising ACF and PACF of a time series called gg_tsdiaply().

vietnam_train %>%

gg_tsdisplay(plot_type='partial')

19.8.2 Visualising Autocorrelations: feasts methods

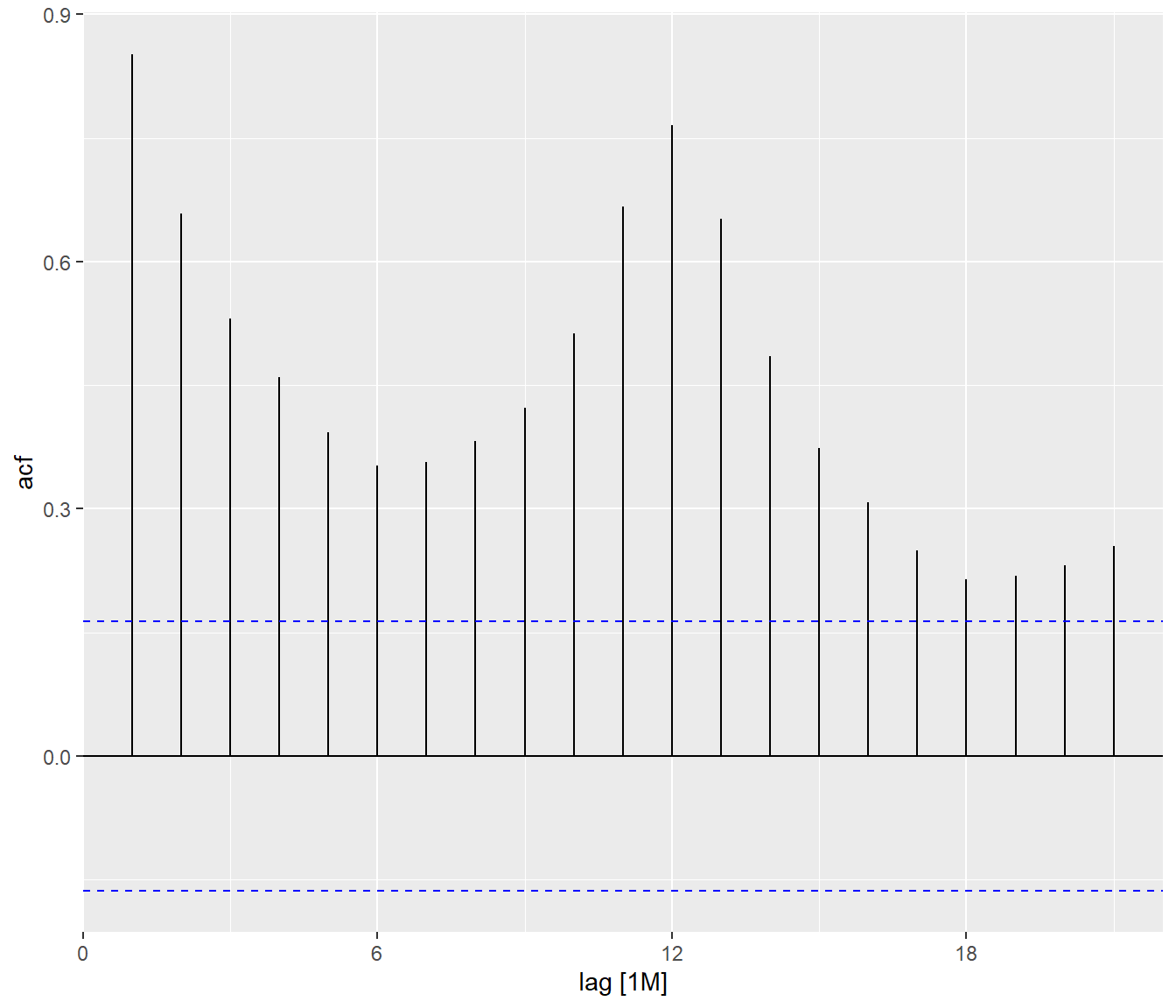

tsibble_longer %>%

filter(`Country` == "Vietnam") %>%

ACF(Arrivals) %>%

autoplot()

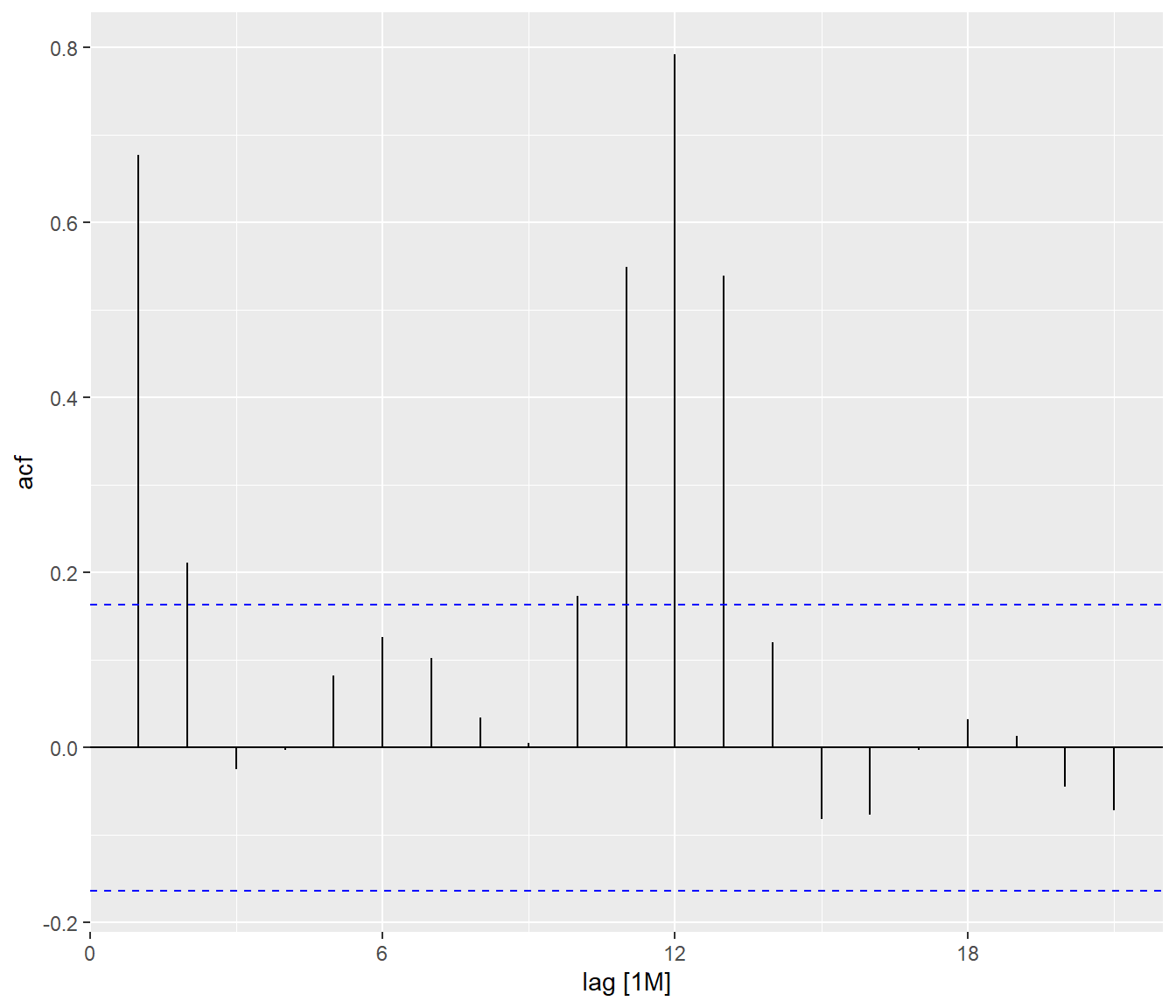

tsibble_longer %>%

filter(`Country` == "United Kingdom") %>%

ACF(Arrivals) %>%

autoplot()

By comparing both ACF plots, it is clear that visitor arrivals from United Kingdom were very seasonal and relatively weaker trend as compare to visitor arrivals from Vietnam.

19.8.3 Differencing: fable methods

19.8.3.1 Trend differencing

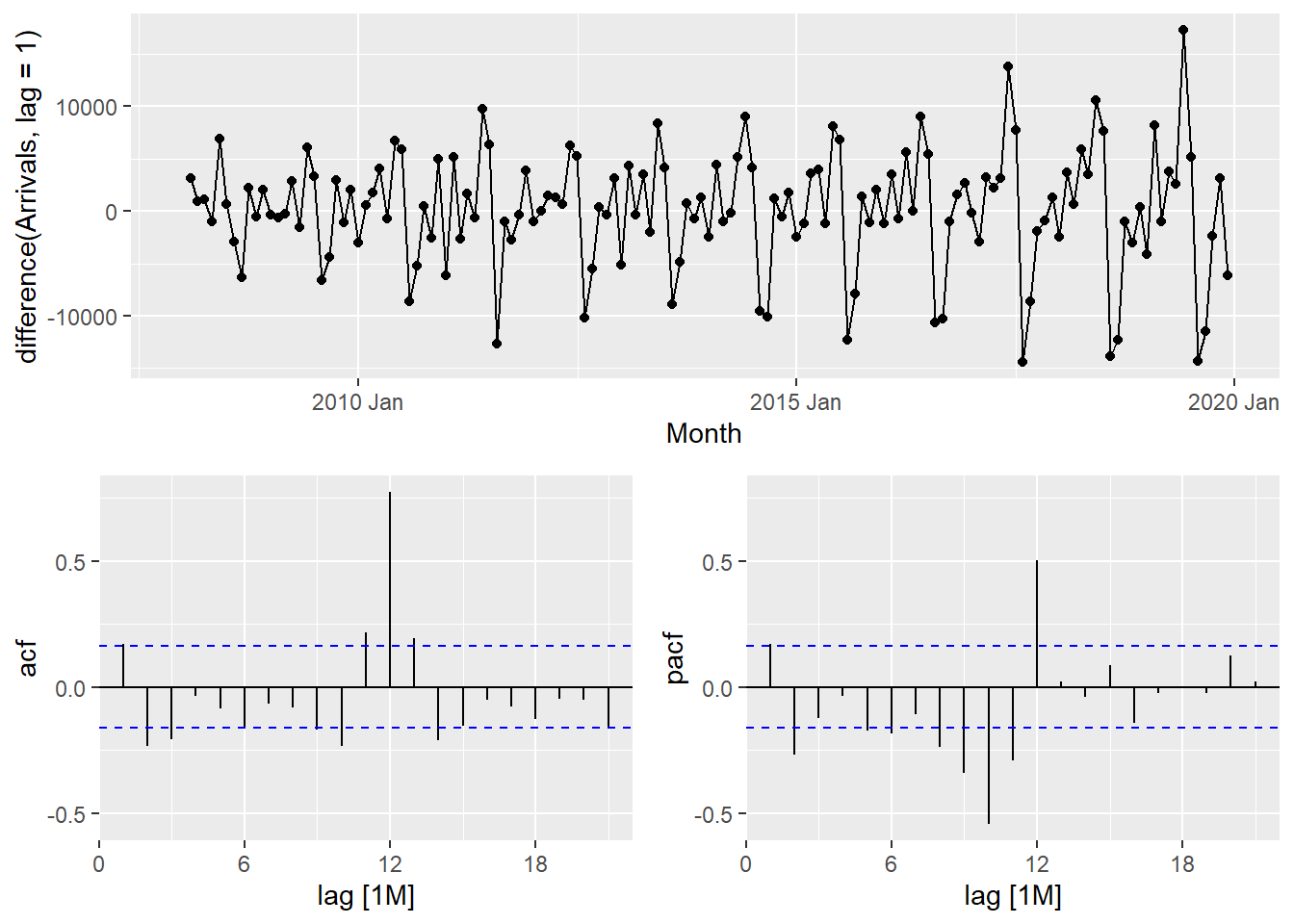

tsibble_longer %>%

filter(Country == "Vietnam") %>%

gg_tsdisplay(difference(

Arrivals,

lag = 1),

plot_type='partial')

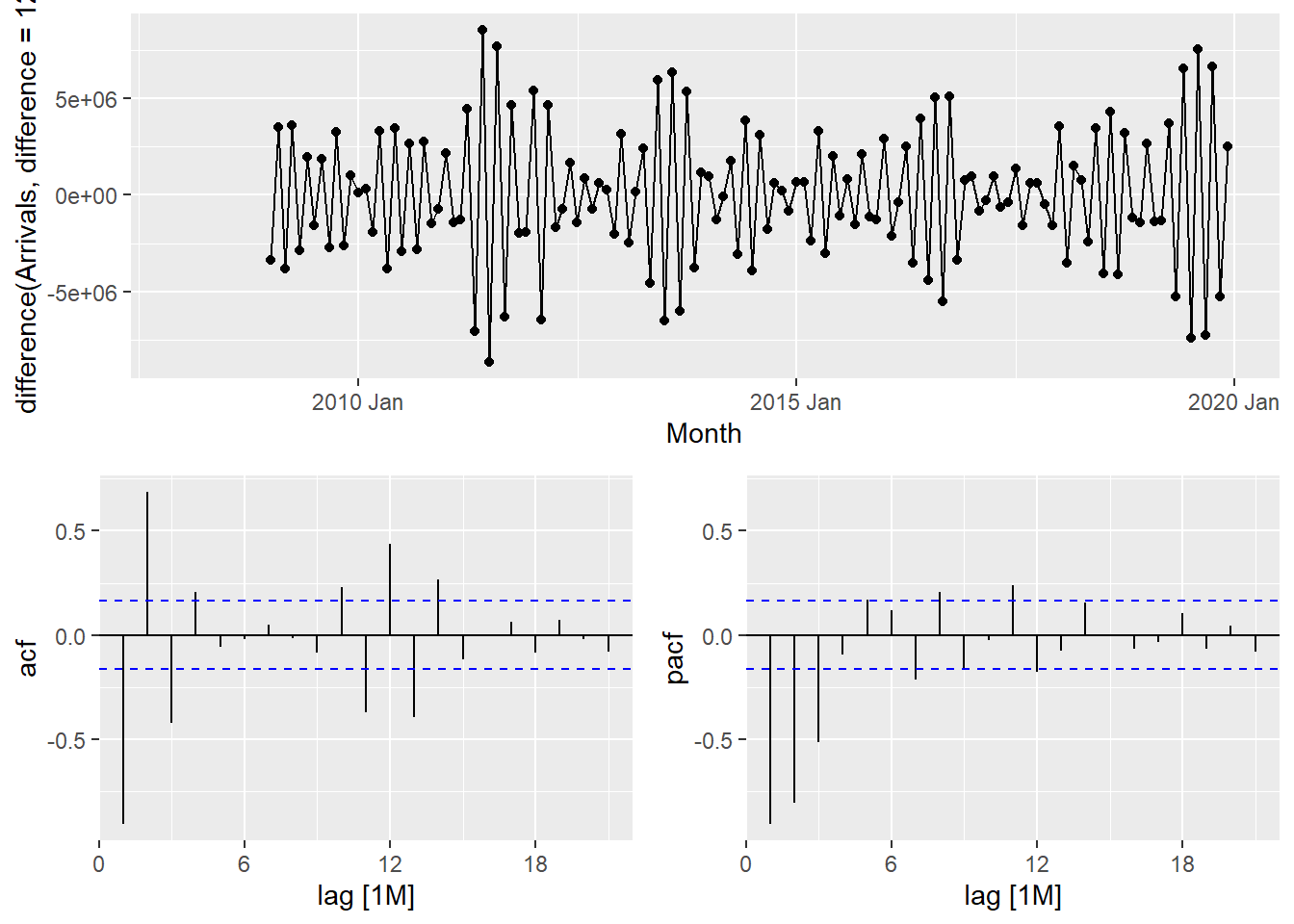

19.8.3.2 Seasonal differencing

tsibble_longer %>%

filter(Country == "Vietnam") %>%

gg_tsdisplay(difference(

Arrivals,

difference = 12),

plot_type='partial')

The PACF is suggestive of an AR(1) model; so an initial candidate model is an ARIMA(1,1,0). The ACF suggests an MA(1) model; so an alternative candidate is an ARIMA(0,1,1).

19.8.4 Fitting ARIMA models manually: fable methods

fit_arima <- vietnam_train %>%

model(

arima200 = ARIMA(Arrivals ~ pdq(2,0,0)),

sarima210 = ARIMA(Arrivals ~ pdq(2,0,0) +

PDQ(2,1,0))

)

report(fit_arima)# A tibble: 2 × 9

Country .model sigma2 log_lik AIC AICc BIC ar_roots ma_roots

<chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <list> <list>

1 Vietnam arima200 4173906. -1085. 2181. 2182. 2198. <cpl [26]> <cpl [0]>

2 Vietnam sarima210 4173906. -1085. 2181. 2182. 2198. <cpl [26]> <cpl [0]>19.8.5 Fitting ARIMA models automatically: fable methods

fit_autoARIMA <- vietnam_train %>%

model(ARIMA(Arrivals))

report(fit_autoARIMA)Series: Arrivals

Model: ARIMA(2,0,0)(2,1,0)[12] w/ drift

Coefficients:

ar1 ar2 sar1 sar2 constant

0.4748 0.1892 -0.5723 -0.1578 1443.2068

s.e. 0.0924 0.0903 0.0989 0.1032 188.9468

sigma^2 estimated as 4173906: log likelihood=-1084.6

AIC=2181.19 AICc=2181.94 BIC=2197.9219.8.6 Model Comparison

bind_rows(

fit_autoARIMA %>% accuracy(),

fit_autoETS %>% accuracy(),

fit_autoARIMA %>%

forecast(h = 12) %>%

accuracy(vietnam_ts),

fit_autoETS %>%

forecast(h = 12) %>%

accuracy(vietnam_ts)) %>%

select(-ME, -MPE, -ACF1)# A tibble: 4 × 8

Country .model .type RMSE MAE MAPE MASE RMSSE

<chr> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl>

1 Vietnam ARIMA(Arrivals) Training 1907. 1458. 5.37 0.491 0.517

2 Vietnam ETS(Arrivals) Training 1745. 1386. 5.29 0.467 0.473

3 Vietnam ARIMA(Arrivals) Test 2647. 2136. 5.17 0.720 0.717

4 Vietnam ETS(Arrivals) Test 3163. 2636. 6.64 0.889 0.85719.8.7 Forecast Multiple Time Series

In this section, we will perform time series forecasting on multiple time series at one goal. For the purpose of the hand-on exercise, visitor arrivals from five selected ASEAN countries will be used.

First, filter() is used to extract the selected countries’ data.

ASEAN <- tsibble_longer %>%

filter(Country == "Vietnam" |

Country == "Malaysia" |

Country == "Indonesia" |

Country == "Thailand" |

Country == "Philippines")Next, mutate() is used to create a new field called Type and populates their respective values. Lastly, filter() is used to extract the training data set and save it as a tsibble object called ASEAN_train.

ASEAN_train <- ASEAN %>%

mutate(Type = if_else(

`Month-Year` >= "2019-01-01",

"Hold-out", "Training")) %>%

filter(Type == "Training")19.8.8 Fitting Mulltiple Time Series

In the code chunk below auto ETS and ARIMA models are fitted by using model().

ASEAN_fit <- ASEAN_train %>%

model(

ets = ETS(Arrivals),

arima = ARIMA(Arrivals)

)19.8.9 Examining Models

The glance() of fabletools provides a one-row summary of each model, and commonly includes descriptions of the model’s fit such as the residual variance and information criteria.

ASEAN_fit %>%

glance()# A tibble: 10 × 12

Country .model sigma2 log_lik AIC AICc BIC MSE AMSE MAE

<chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 Indonesia ets 1.02e-2 -1561. 3156. 3161. 3205. 1.74e8 1.80e8 0.0732

2 Indonesia arima 1.48e+8 -1290. 2589. 2590. 2603. NA NA NA

3 Malaysia ets 4.67e-3 -1430. 2894. 2899. 2943. 2.04e7 2.00e7 0.0506

4 Malaysia arima 2.62e+7 -1185. 2378. 2379. 2390. NA NA NA

5 Philippines ets 3.56e-3 -1343. 2722. 2728. 2774. 5.28e6 7.58e6 0.0461

6 Philippines arima 8.04e+6 -1122. 2260. 2262. 2283. NA NA NA

7 Thailand ets 6.63e-3 -1343. 2722. 2728. 2774. 5.40e6 6.33e6 0.0584

8 Thailand arima 8.51e+6 -1127. 2269. 2270. 2288. NA NA NA

9 Vietnam ets 4.55e-3 -1300. 2635. 2640. 2684. 3.05e6 3.42e6 0.0520

10 Vietnam arima 4.17e+6 -1085. 2181. 2182. 2198. NA NA NA

# ℹ 2 more variables: ar_roots <list>, ma_roots <list>Be wary though, as information criteria (AIC, AICc, BIC) are only comparable between the same model class and only if those models share the same response (after transformations and differencing).

19.8.10 Extracintg fitted and residual values

The fitted values and residuals from a model can obtained using fitted() and residuals() respectively. Additionally, the augment() function may be more convenient, which provides the original data along with both fitted values and their residuals.

ASEAN_fit %>%

augment()# A tsibble: 1,320 x 7 [1M]

# Key: Country, .model [10]

Country .model Month Arrivals .fitted .resid .innov

<chr> <chr> <mth> <dbl> <dbl> <dbl> <dbl>

1 Indonesia ets 2008 Jan 62683 56534. 6149. 0.109

2 Indonesia ets 2008 Feb 47834 46417. 1417. 0.0305

3 Indonesia ets 2008 Mar 64688 62660. 2028. 0.0324

4 Indonesia ets 2008 Apr 58074 61045. -2971. -0.0487

5 Indonesia ets 2008 May 57089 62280. -5191. -0.0833

6 Indonesia ets 2008 Jun 70118 75791. -5673. -0.0749

7 Indonesia ets 2008 Jul 73805 78691. -4886. -0.0621

8 Indonesia ets 2008 Aug 58015 61910. -3895. -0.0629

9 Indonesia ets 2008 Sep 63730 74518. -10788. -0.145

10 Indonesia ets 2008 Oct 71206 67869. 3337. 0.0492

# ℹ 1,310 more rows19.8.11 Comparing Fit Models

In the code chunk below, accuracy() is used to compare the performances of the models.

ASEAN_fit %>%

accuracy() %>%

arrange(Country)# A tibble: 10 × 11

Country .model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

<chr> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 Indonesia ets Trai… -1.81e3 13187. 9665. -1.83 7.57 0.556 0.619 -0.236

2 Indonesia arima Trai… -9.54e1 11351. 8382. -0.136 6.38 0.482 0.533 -0.00802

3 Malaysia ets Trai… -6.78e2 4515. 3538. -1.25 5.15 0.529 0.527 -0.288

4 Malaysia arima Trai… -2.33e1 4801. 3684. -0.109 5.20 0.551 0.561 -0.00933

5 Philippi… ets Trai… -2.35e0 2298. 1897. -0.334 4.64 0.464 0.408 0.0400

6 Philippi… arima Trai… 9.53e0 2624. 1934. -0.269 4.60 0.473 0.466 0.00717

7 Thailand ets Trai… 1.97e1 2323. 1773. -0.511 5.89 0.489 0.485 -0.0812

8 Thailand arima Trai… 5.88e1 2710. 1932. -0.562 6.16 0.532 0.565 -0.0112

9 Vietnam ets Trai… -3.52e1 1745. 1386. -0.728 5.29 0.467 0.473 0.279

10 Vietnam arima Trai… 1.95e0 1907. 1458. -0.671 5.37 0.491 0.517 0.0136 19.8.12 Forecast Future Values

Forecasts from these models can be produced directly as our specified models do not require any additional data.

ASEAN_fc <- ASEAN_fit %>%

forecast(h = "12 months")19.8.13 Visualising the forecasted values

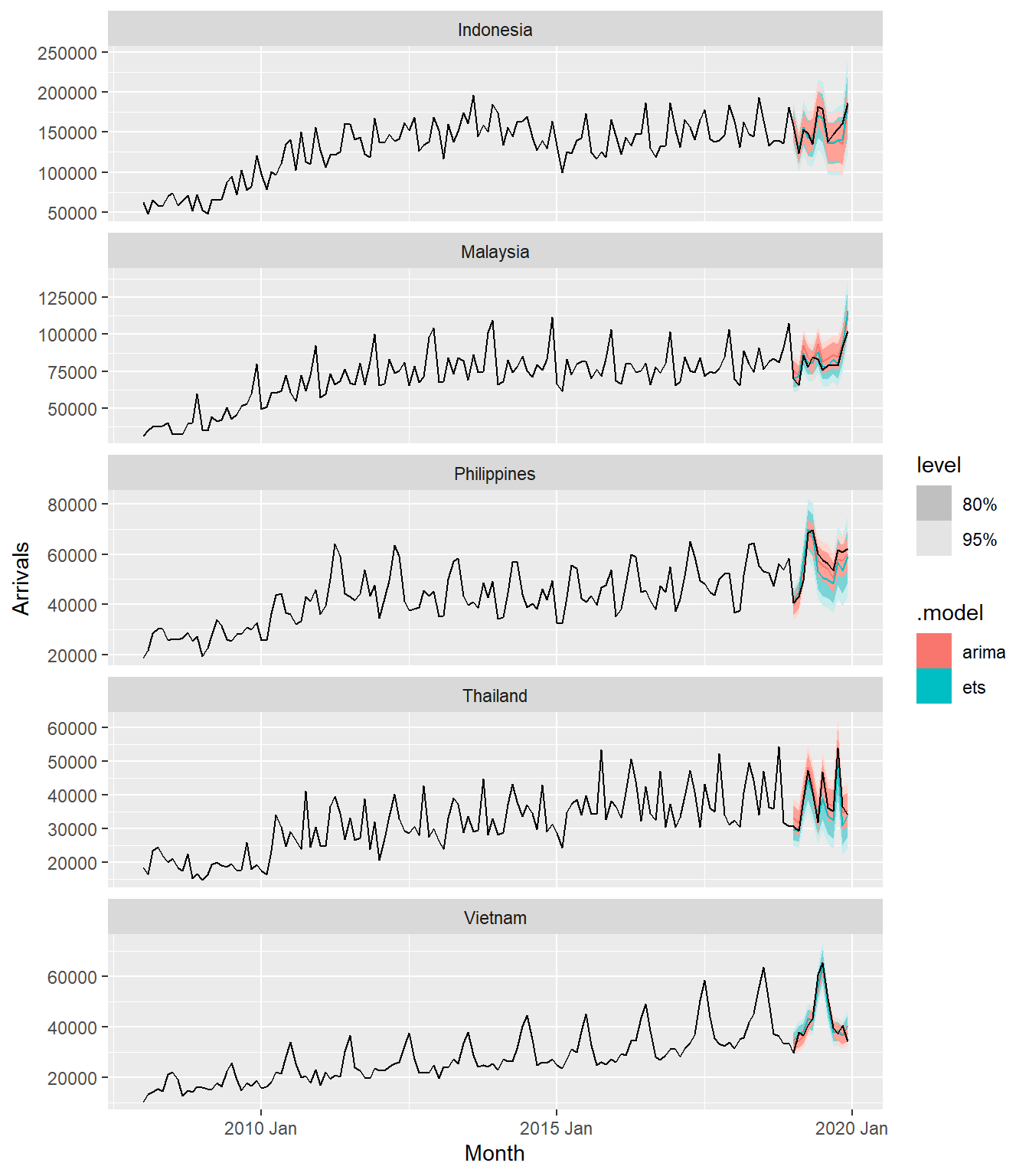

In the code chunk below autoplot() of feasts package is used to plot the raw and fitted values.

ASEAN_fc %>%

autoplot(ASEAN)

19.9 Reference

Rob J Hyndman and George Athanasopoulos (2022) Forecasting: Principles and Practice (3rd ed), online version.